Equity Management: A Complete Guide for Investors

Equity Management: A Complete Guide for Investors

Managing ownership stakes across investment portfolios requires precision, transparency, and systematic coordination. Whether you're tracking capital contributions for a multifamily syndication, calculating waterfall distributions across multiple real estate assets, or reporting to limited partners on their ownership positions, equity management forms the operational backbone of professional investment firms. The challenge intensifies when ownership data lives scattered across legal documents, financial models, property management systems, and investor communications. For firms managing commercial real estate portfolios or multi-asset investment vehicles, the complexity multiplies with each new deal, partner structure, and reporting requirement.

Understanding Equity Management in Investment Operations

Equity management encompasses all processes related to tracking, administering, and reporting on ownership interests within investment vehicles and individual assets. This includes documenting who owns what percentage of which entities, recording capital contributions and distributions, calculating returns according to agreed-upon formulas, and maintaining accurate records for tax, legal, and operational purposes.

In real estate and alternative investments, equity management extends beyond simple ownership percentages. You must track multiple layers of entities, understand preferred return structures, manage promote calculations, coordinate with lenders on equity requirements, and ensure compliance with partnership agreements.

Core Components of Investment Equity Structures

The foundation of effective equity management starts with properly documented ownership structures. Each investment vehicle requires clear documentation of:

Entity formation documents specifying ownership classes and governance rights

Operating agreements detailing capital call procedures and distribution priorities

Subscription agreements capturing each investor's commitment and funding schedule

Side letters documenting special terms negotiated with specific investors

Amendment documentation tracking changes to ownership or economic terms over time

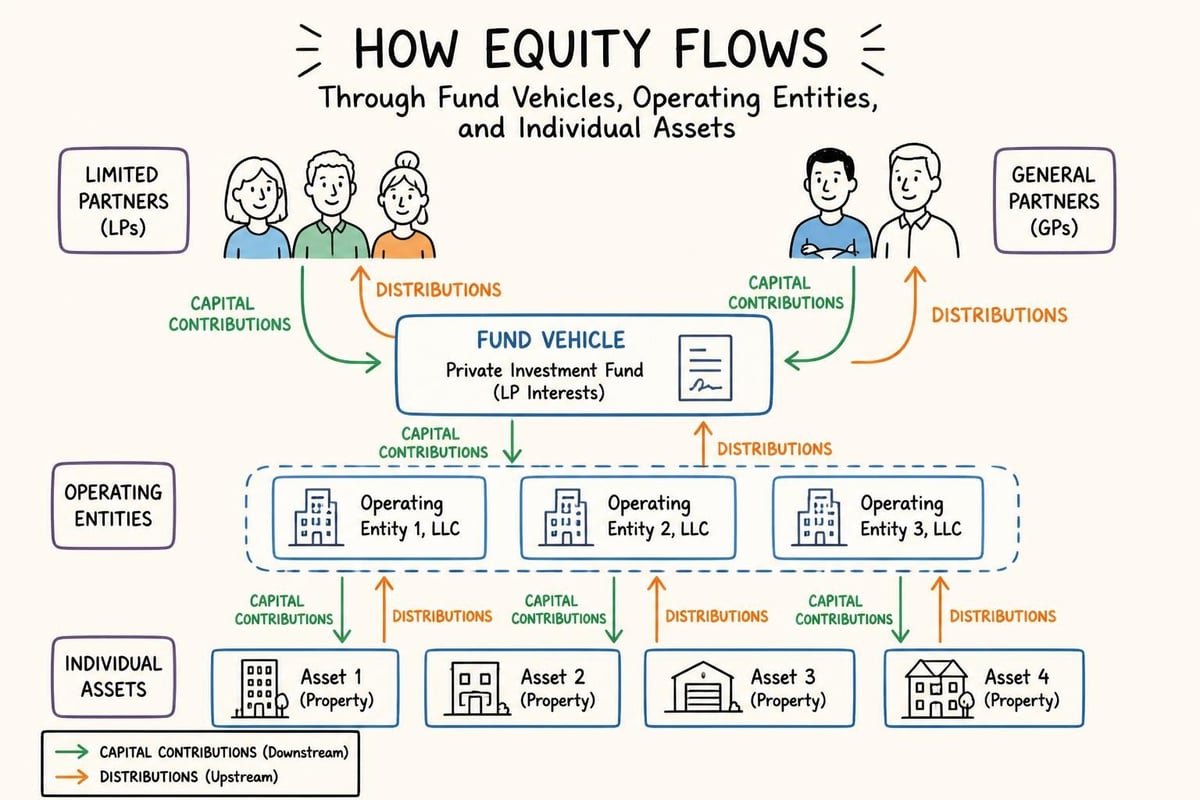

Most institutional investment firms operate through multi-tiered structures where a fund entity owns operating companies, which in turn own individual properties or portfolio companies. Best practices in equity management emphasize maintaining clear, accessible records of these ownership chains to support accurate reporting and decision-making.

Capital Contribution Tracking and Management

Tracking capital contributions represents a fundamental equity management responsibility. Each time investors fund a capital call, you must record the amount, date, source investor, and destination asset or entity. This creates an audit trail supporting future distribution calculations and tax reporting.

Consider a commercial real estate fund acquiring three office buildings over 18 months. Each acquisition triggers capital calls to limited partners based on their commitment percentages. Some investors may have different commitment amounts across multiple closings. Others might hold co-investment rights allowing additional capital beyond their fund commitment.

Your equity management system must track:

Initial commitments and any modifications through side letters

Capital call notices sent and responses received

Actual funding dates and amounts for each investor

Allocation of contributed capital to specific investments

Unfunded commitments remaining for each investor

Default provisions if investors fail to fund called capital

Without systematic tracking, you cannot accurately calculate each investor's ownership percentage, which shifts with each capital event when investors fund at different rates or exercise co-investment rights.

Waterfall Structures and Distribution Calculations

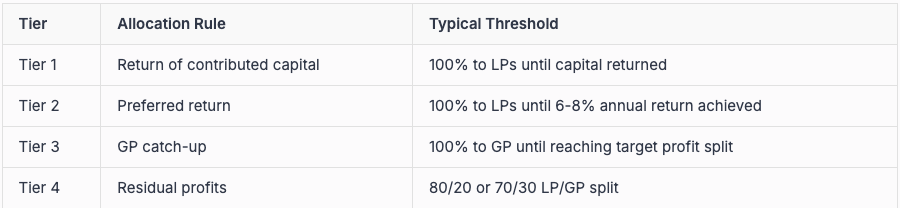

Distribution waterfalls define how cash flows from operations and sales move from the asset level up through entities to individual investors. These structures typically include preferred returns, return of capital hurdles, and carried interest (promote) allocations to sponsors.

Common Waterfall Tier Structures

Most real estate and private equity waterfalls follow a tiered approach where distributions flow sequentially through defined hurdles:

The complexity compounds when managing multiple assets with different waterfall structures, investor-specific terms, or hybrid calculation methods combining European and American waterfall concepts.

Management equity plans in real estate and investment contexts often include carried interest provisions that require precise calculation across changing portfolio values and investor bases.

Calculating Returns Across Multiple Time Periods

Equity management requires calculating investor returns accurately across various time horizons. You must track internal rates of return (IRR), equity multiples, and cash-on-cash returns both at the individual investment level and across the entire portfolio.

For quarterly reporting, you need systems that can:

Calculate unrealized value changes based on updated asset valuations

Determine each investor's share of unrealized gains or losses

Track realized gains from asset sales or refinancings

Allocate income and expenses according to ownership percentages and tax agreements

Generate investor-specific performance metrics reflecting their unique entry dates and capital contribution timing

The mathematical precision required for these calculations makes manual Excel-based approaches increasingly risky as portfolio complexity grows.

Investor Obligations and Rights Management

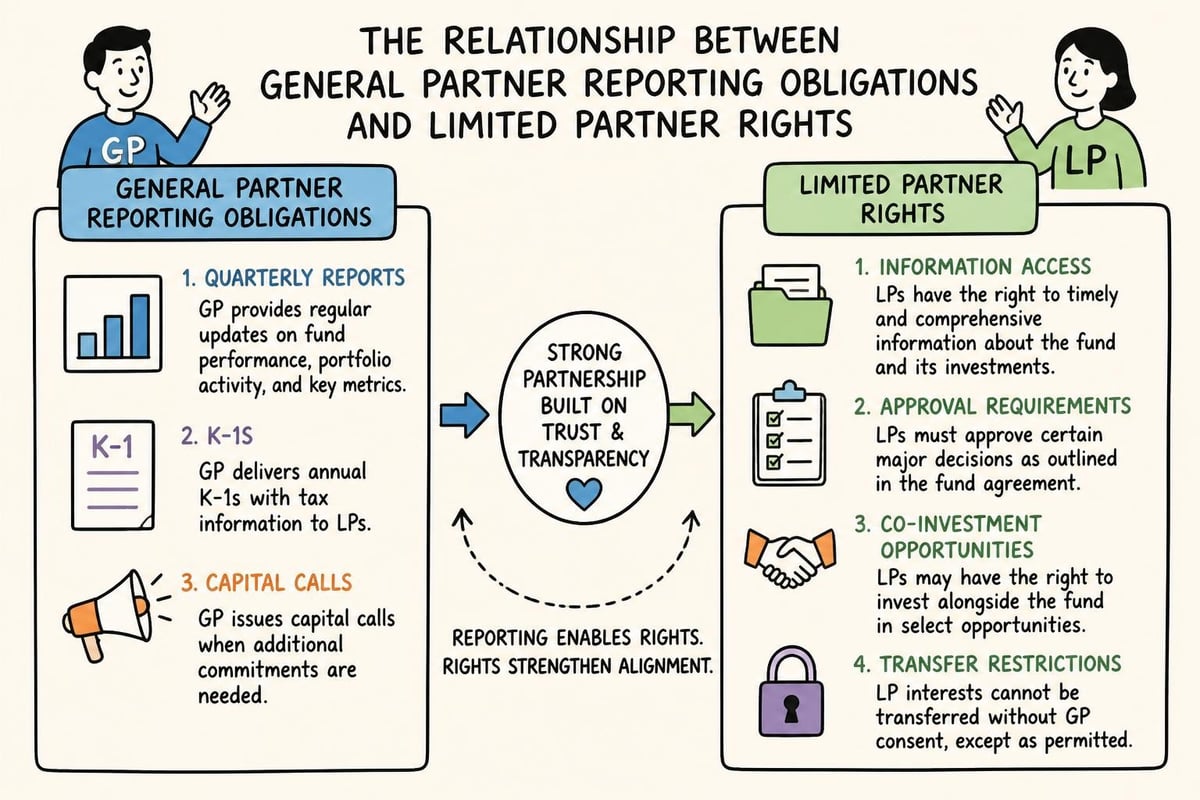

Beyond economic calculations, equity management encompasses tracking and fulfilling investor obligations outlined in governing documents. These obligations extend in both directions between general partners and limited partners.

GP Obligations to Limited Partners

General partners maintain specific responsibilities requiring systematic tracking:

Quarterly financial reporting with balance sheets, income statements, and cash flow details for each fund and underlying asset

Annual audited financial statements coordinated with external auditors

Tax package delivery including K-1s and supporting schedules by regulatory deadlines

Material event notifications about acquisitions, dispositions, financings, or litigation

Annual meetings or investor calls reviewing performance and strategy

Capital call notices providing adequate advance notice before funding deadlines

Firms using AI for portfolio management can automate much of the data aggregation supporting these reporting obligations, reducing manual effort while improving accuracy.

LP Rights Requiring Tracking Systems

Limited partners hold specific rights requiring proactive management by the general partner:

Information rights allowing inspection of books and records

Approval rights for major decisions like asset sales or refinancings

Co-investment opportunities offered according to side letter terms

Transfer restrictions governing when and how LP interests can be sold

Redemption rights in open-end fund structures

Advisory committee participation for LPs meeting size thresholds

Missing a co-investment notification deadline or failing to obtain required approvals creates legal exposure and damages investor relationships. Systematic equity management prevents these operational failures.

Data Fragmentation Challenges in Equity Management

The operational reality for most investment firms involves equity-related information scattered across disconnected systems and document repositories. Legal agreements live in document management systems, financial models exist in Excel spreadsheets, accounting data sits in specialized software, and investor communications reside in email archives or CRM platforms.

This fragmentation creates multiple pain points:

Version control issues arise when partnership agreements get amended but the changes don't flow into financial models calculating distributions. One team references outdated waterfall terms while another uses the current structure, leading to conflicting investor reports.

Manual reconciliation burden consumes significant time as analysts cross-reference legal documents against accounting records to verify capital contributions, compare modeled distributions to actual payments, and validate investor ownership percentages across systems.

Audit trail gaps emerge when the connection between a legal term and its implementation in financial calculations remains undocumented. During audits or investor due diligence, teams scramble to demonstrate how specific provisions translate into reported numbers.

Why Traditional Systems Fall Short

Property management systems and accounting platforms excel at transaction recording but lack the contextual understanding to interpret partnership agreements or calculate complex waterfalls. They store data but don't connect legal provisions to financial outcomes.

Static cap table software designed for startups focuses on employee option pools and simple equity classes, missing the nuanced waterfall structures, multi-tiered entities, and investor-specific provisions common in real estate and institutional investment management.

Excel models provide flexibility but become unwieldy at portfolio scale, lack audit trails, require manual updates, and create version control nightmares when multiple team members maintain separate workbooks.

Portfolio-Level Equity Decision Making

Sophisticated investment firms make decisions considering equity implications across their entire portfolio rather than viewing each asset in isolation. This requires integrated equity management systems that surface relationships and trade-offs.

Asset-Level Decisions with Portfolio Implications

When evaluating whether to sell an individual property, you must consider how that sale affects:

Fund-level IRR and equity multiple metrics that determine GP promote calculations

Investor-specific return thresholds where selling one asset might trigger waterfall tier shifts

Entity-level tax consequences including depreciation recapture and capital gains allocation

Reinvestment period status affecting whether sale proceeds can deploy into new acquisitions

Fundraising positioning as current fund performance influences next fund commitments

Teams using portfolio strategy approaches need equity management systems that model these interconnections, not just isolated asset analysis.

Equity Risk Visibility Across Assets

Effective equity management provides visibility into concentration risks and exposure patterns across the portfolio:

Which investors have the largest aggregate commitments across multiple funds?

How much unfunded capital remains callable if new opportunities arise?

What percentage of the portfolio sits in assets approaching waterfall hurdles that change distribution economics?

Which investments have investor-specific terms creating complexity or misalignment?

Where do entity structures create tax inefficiencies or operational bottlenecks?

Commercial real estate portfolio management increasingly requires this integrated view connecting equity structures to portfolio outcomes.

Equity Reporting Automation and Accuracy

Investor reporting represents the most visible output of equity management processes. Quarterly reports must accurately reflect each investor's capital account, distributions received, unrealized value, and performance metrics. Errors damage credibility and create administrative burden addressing investor questions.

Components of Comprehensive Investor Reporting

Professional investor reports typically include:

Capital account reconciliation showing beginning balance, contributions, distributions, and income/loss allocation

Performance metrics including IRR, equity multiple, and cash yield calculations

Asset-level detail for each property or investment in the portfolio

Market commentary contextualizing performance against broader trends

Pipeline updates describing potential acquisitions or dispositions

Fee calculations transparently showing management fees and performance allocations

Generating these reports manually from disparate data sources creates a multi-week production cycle each quarter. Equity compensation professionals in the corporate context face similar challenges coordinating data across systems.

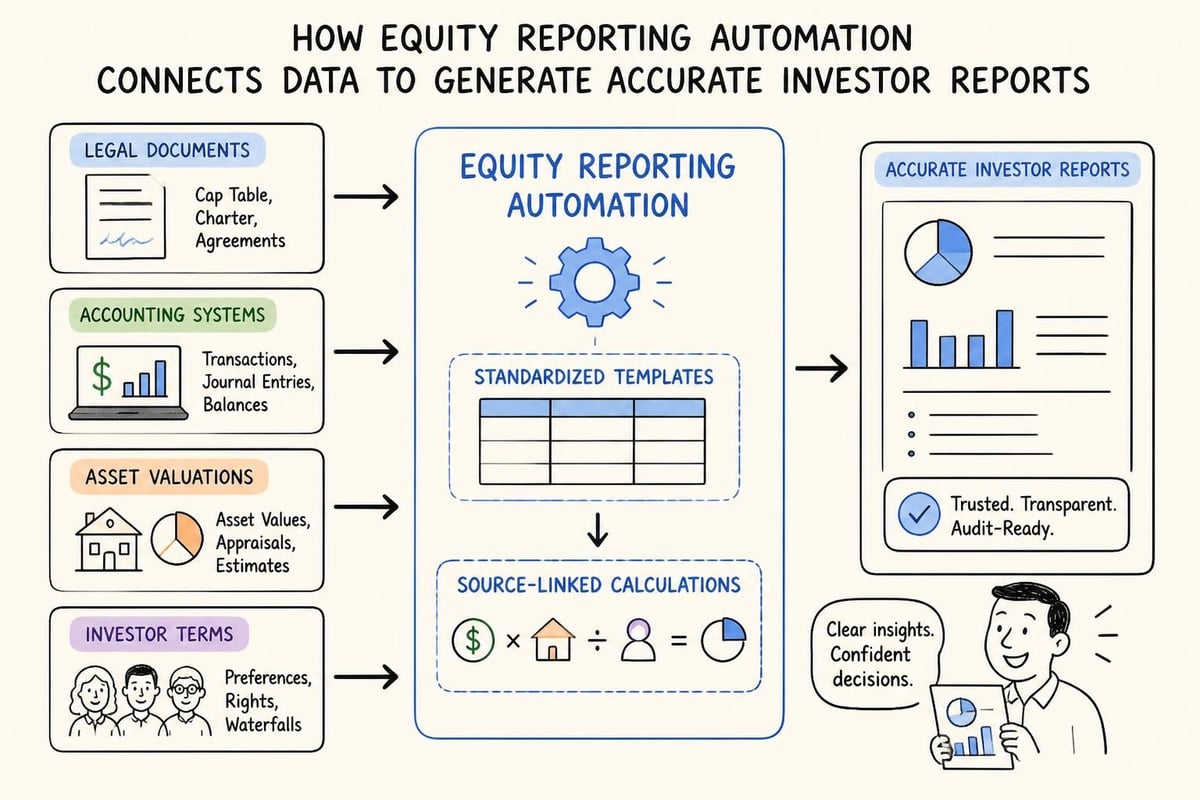

Automating Recurring Reporting Workflows

Modern approaches to equity management leverage automation to reduce reporting cycle times while improving accuracy. This involves:

Data integration pipelines that pull information from accounting systems, property management platforms, and valuation models into a central reporting environment.

Template-based report generation where standardized formats automatically populate with current data, highlighting period-over-period changes and flagging anomalies for review.

Source-linked calculations that maintain audit trails connecting every reported number back to underlying transactions and agreements, enabling rapid verification during investor questions.

Exception flagging that surfaces unusual patterns like distribution amounts inconsistent with waterfall terms or capital account balances that don't reconcile to contributed capital and allocated income.

Teams implementing these approaches using tools for data analysis can compress reporting cycles from weeks to days while reducing error rates.

Advanced Equity Management Considerations

As investment firms scale, equity management complexity increases beyond basic tracking and reporting. Advanced topics requiring systematic approaches include:

Tax Basis Tracking and K-1 Preparation

Partnership tax reporting requires tracking each investor's tax basis separately from their capital account. Tax basis adjusts for allocated income and losses, tax-exempt income, and nondeductible expenses in ways that differ from book capital accounts.

Generating accurate Schedule K-1s demands:

Separate tracking of ordinary income, capital gains, and tax-exempt income

Allocation of expenses between deductible and nondeductible categories

Application of partnership audit rules (BBA vs. TEFRA)

State-level tax reporting for multi-state property portfolios

Compliance with basis limitation rules and at-risk provisions

This specialized knowledge area often requires coordination between equity management systems and tax preparation software, with substantial manual intervention for complex situations.

Transfer Restrictions and Secondary Markets

Most investment partnerships restrict LP interest transfers to maintain investor quality and avoid regulatory issues. Equity management must track:

Approval requirements where transfers need GP or advisory committee consent

Right of first refusal provisions giving other investors purchase rights

Lock-up periods preventing transfers for specified time frames

Qualified transferee standards restricting purchasers to accredited investors or qualified purchasers

Transfer pricing using valuation policies to determine secondary transaction values

As secondary markets for private investment interests grow, systematic management of these provisions becomes increasingly important.

Co-Investment Waterfalls and Aggregation

When investors hold both fund interests and asset-specific co-investments, calculating returns requires aggregating across multiple positions with different waterfall terms. An investor might participate in the main fund receiving an 8% preferred return and 80/20 profit split while holding a separate co-investment with a 6% preferred return and 90/10 split.

Accurate reporting means calculating each position separately, then aggregating to show the investor's total relationship performance. This becomes exponentially complex with multiple co-investments across different vintage years and structures.

Connecting Equity Management to Operational Excellence

The ultimate purpose of sophisticated equity management extends beyond compliance and reporting. It enables better decision-making by connecting ownership structures to operational and strategic choices.

When acquisition teams evaluate new investments, equity management systems should instantly model how adding that asset affects fund-level metrics, whether unfunded capital supports the purchase, and how the investment fits within concentration limits or strategy mandates.

When asset managers consider capital improvements, they need visibility into how those investments affect investor returns through their impact on valuations, cash flows, and ultimate exit pricing.

When investor relations teams negotiate terms for new funds, historical equity management data informs competitive positioning and identifies which provisions create operational complexity worth avoiding in future structures.

Firms investing in real estate equity investment capabilities recognize that equity management forms the connective tissue between legal structures, financial performance, and stakeholder relationships.

The Role of AI in Modern Equity Management

Artificial intelligence offers transformative potential for equity management by connecting documents to data, automating routine analysis, and surfacing insights buried in complex agreements and transaction histories.

AI systems can read partnership agreements and automatically extract waterfall terms, capital call provisions, and investor-specific rights into structured data. This eliminates manual abstraction and ensures operational teams work from current, accurate information about equity structures.

Natural language interfaces allow team members to query equity data conversationally: "Which investors haven't funded their full commitment?" or "What's our aggregate exposure to investors based in California?" The system retrieves answers by analyzing structured data and unstructured documents together.

Anomaly detection algorithms flag inconsistencies between legal agreements and implemented calculations, such as waterfall distributions that don't match documented terms or capital accounts that fail to reconcile across systems. This proactive identification prevents errors before they reach investor reports.

These capabilities become practical when AI systems connect to comprehensive data across legal documents, financial models, accounting records, and investor communications. The integration enables analysis that would require weeks of manual research to complete.

Effective equity management requires systematic coordination across legal structures, financial calculations, investor obligations, and portfolio-level decision-making. As investment portfolios grow in complexity, firms need integrated approaches that connect documents and data while automating routine workflows and surfacing insights that inform strategic choices. Leni serves as an AI analyst layer for investment teams, connecting disparate data sources, summarizing complex agreements, supporting source-linked analysis, and automating recurring equity reporting tasks so professionals can focus on value-added decision-making rather than manual data wrangling.

Curious About AI?

Join the largest AI community for real estate online. Get bite-sized, real-world use case videos, plus practical tips and proven strategies from top industry experts on adopting AI effectively.

MEET LENI

AI SuperAgent Purpose Built for Investors and Operators.

Experience how professionals and teams in your domain are getting the edge using AI.