Multifamily Underwriting Tool: Complete Guide for 2026

Multifamily Underwriting Tool: Complete Guide for 2026

The commercial real estate industry's underwriting process hasn't kept pace with the complexity of modern multifamily investments. While deal sizes have grown and investor expectations have become more sophisticated, most acquisitions teams still rely on manual data extraction, disconnected spreadsheets, and hours of comp research that could be automated. The bottleneck isn't the financial model itself but the data layer beneath it. A purpose-built multifamily underwriting workflow addresses this fundamental problem by structuring the entire path from document intake to final deliverable. Underwriting is one of the clearest back-office workflows where specialized AI can reduce manual cost while preserving verifiable accuracy.

Understanding the Multifamily Underwriting Workflow

Traditional underwriting follows a predictable sequence that consumes dozens of hours per deal. Acquisitions teams receive property documents, extract financial data manually, build assumptions from market research, construct financial models, and package findings for investment committees.

The typical workflow breaks down into five distinct stages:

Document collection and initial review

Financial data extraction and validation

Market research and comparable property analysis

Financial modeling and scenario testing

Investment committee package preparation

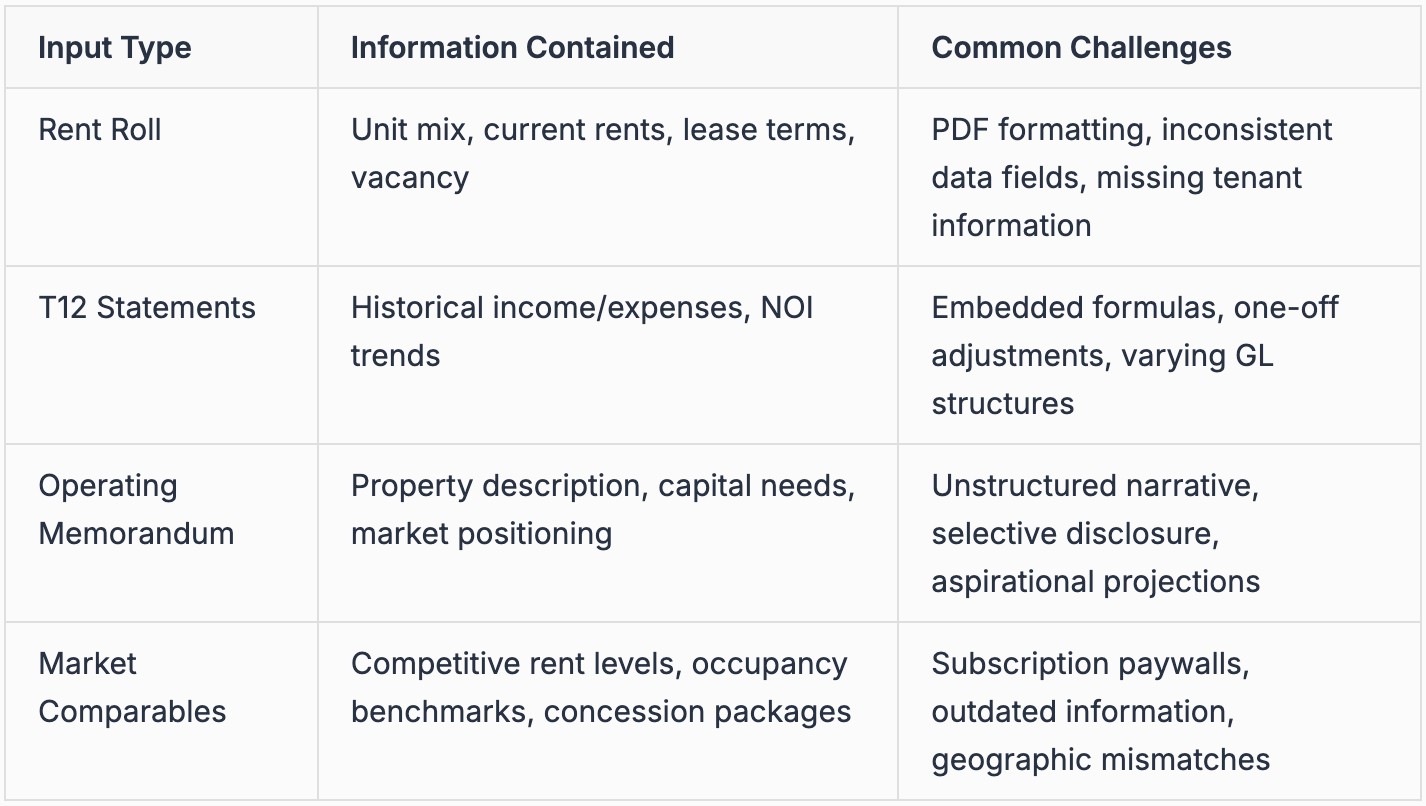

Each stage introduces potential failure points. Rent rolls arrive as PDFs with inconsistent formatting. T12 operating statements contain embedded formulas that don't match reported figures. Market data lives across multiple platforms with different subscription costs and access limitations.

The time lost at the data layer compounds throughout the process. An analyst spending three hours extracting rent roll data manually introduces transcription errors that propagate through every subsequent calculation. These errors only surface during final reconciliation, forcing teams to backtrack and rebuild models under deadline pressure.

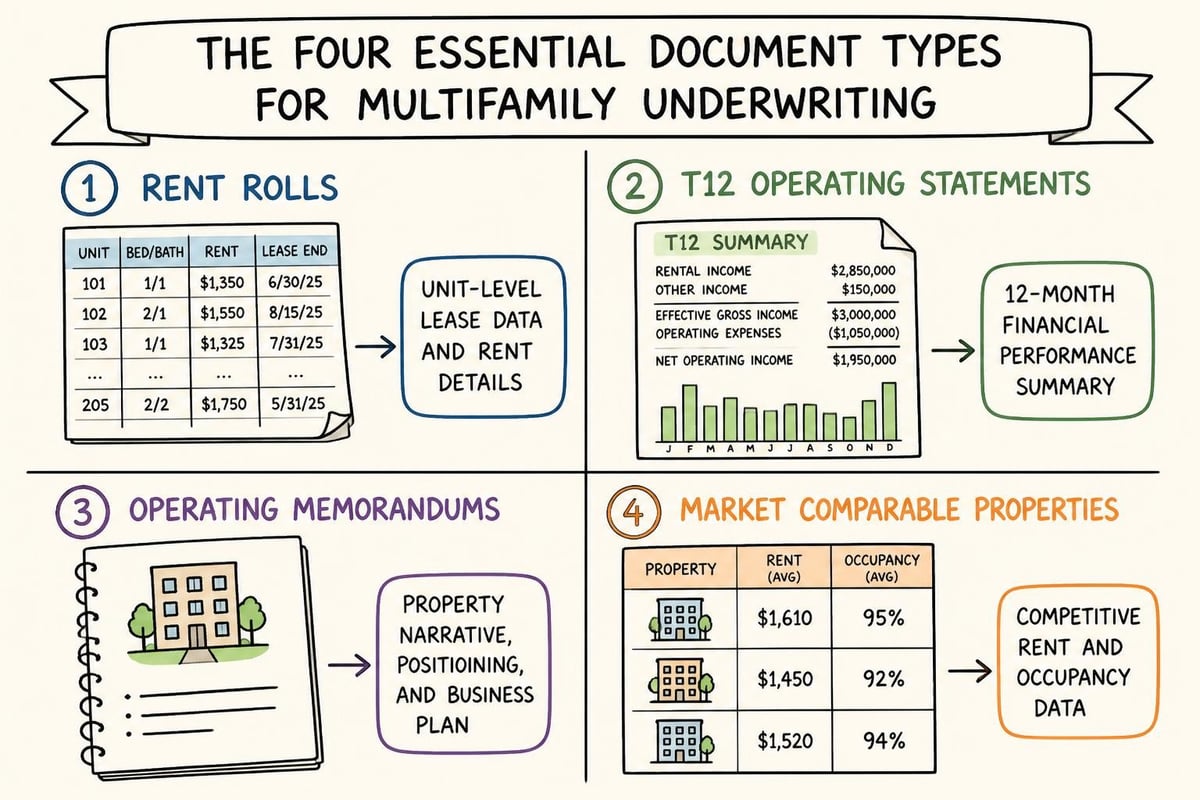

Critical Inputs Required for Multifamily Underwriting

Every multifamily underwriting exercise demands the same core dataset. Without complete, accurate inputs, the analysis becomes speculation rather than rigorous financial assessment.

A comprehensive multifamily underwriting tool must handle all these document types without requiring manual reformatting. The tool should recognize that rent rolls from different property management systems follow different schemas but contain the same underlying information.

Where Traditional Approaches Break Down

Most acquisitions teams cobble together workflows using general-purpose tools never designed for real estate underwriting. Excel handles calculations but not document extraction. ChatGPT drafts assumption narratives but can't verify figures against source documents. Dedicated research platforms provide market data but don't integrate with financial models.

Manual Extraction Creates Compounding Delays

The average multifamily rent roll contains 100-300 units with 15-20 data points per unit. Manual extraction requires opening the PDF, creating a matching spreadsheet structure, and transcribing 1,500-6,000 individual data points. This process alone consumes four to eight hours for a typical deal.

Errors emerge immediately. Unit numbers get transposed. Lease expiration dates default to incorrect formatting. Square footage figures include commas that Excel interprets as text. Each error requires identification, correction, and model recalculation.

Common extraction pain points include:

Inconsistent date formats across different lease vintages

Embedded images or watermarks disrupting PDF text selection

Multi-page rent rolls with repeating headers that interrupt data continuity

Calculated fields that show formulas rather than values when copied

The same challenges apply to T12 extraction. Operating statements arrive with custom general ledger structures that don't map cleanly to standard income and expense categories. One property lists "Repairs and Maintenance" as a single line item while another breaks it into "Unit Turns," "HVAC Service," "Plumbing," and "Grounds Maintenance."

Market Research Fragmentation Slows Comp Analysis

Comparable property research typically requires subscriptions to CoStar, Yardi Matrix, and local brokerage databases. Each platform uses different geographic boundaries, property classifications, and reporting periods. An analyst building a comp set must access multiple systems, export data in different formats, and manually reconcile discrepancies.

The research itself follows no standardized methodology. Which properties qualify as comparable? Should the comp set prioritize geographic proximity, vintage similarity, or amenity matching? Different analysts apply different criteria, producing inconsistent results that complicate deal comparison across a portfolio.

Generic AI tools provide helpful summaries but lack verifiable sourcing. A language model might confidently state that average Class A rents in a submarket are $2.85 per square foot, but the figure cannot be traced back to a specific report or data pull. Investment committees increasingly demand source-linked research that can withstand investor due diligence.

Assumption Building Lacks Institutional Memory

Every underwriting requires dozens of assumptions about rent growth, expense escalation, capital expenditure timing, and exit cap rates. Experienced teams develop internal benchmarks based on portfolio performance, but this institutional knowledge lives in individual analysts' heads rather than accessible systems.

New team members start from zero. They review comparable assumptions from previous deals, but context gets lost. Why did the team underwrite 3% annual rent growth on one deal but 4.5% on another? Were the properties truly different, or did market conditions shift between analyses?

A proper multifamily underwriting tool captures this institutional knowledge systematically. As teams complete more deals, the platform learns which assumptions proved accurate and which required adjustment. Commercial real estate analytics become portable rather than personal.

Components of a Complete Underwriting Package

Investment committees expect standardized deliverables that support informed capital allocation decisions. The underwriting package serves as both analytical tool and communication document, translating property-level detail into portfolio-level strategy.

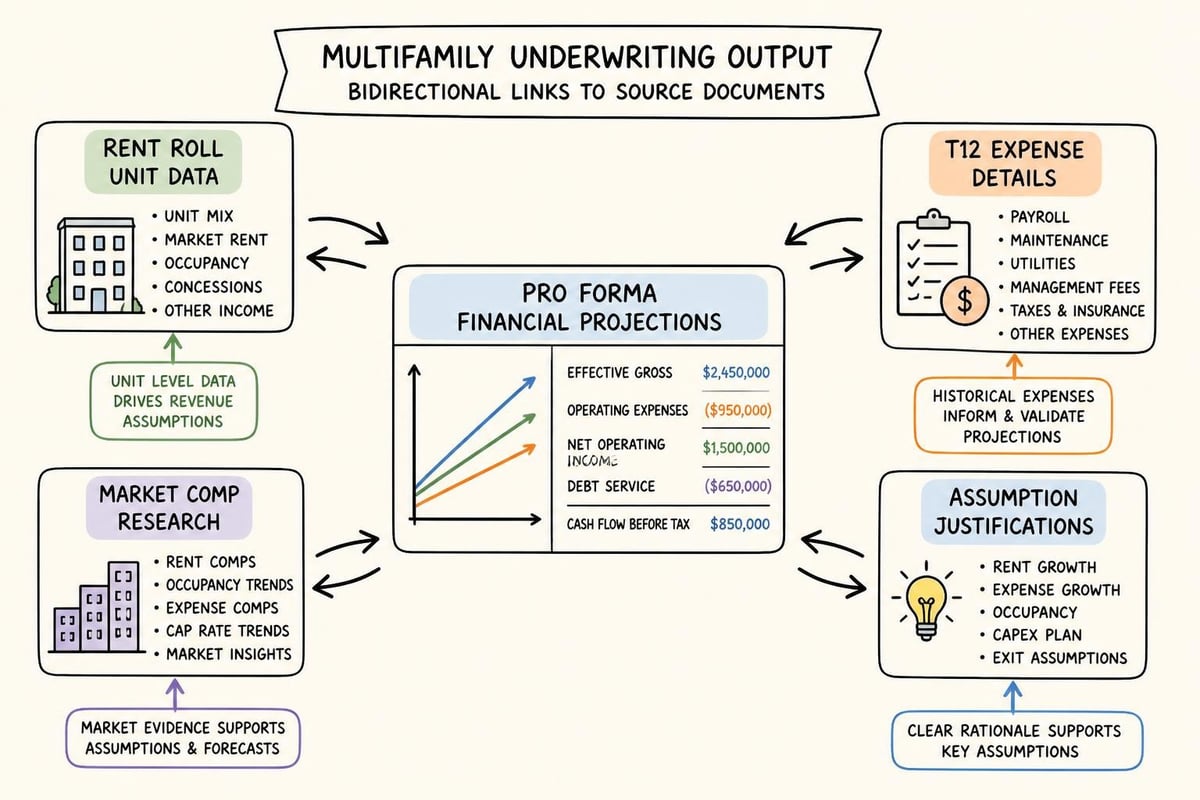

Pro Forma Financial Projections

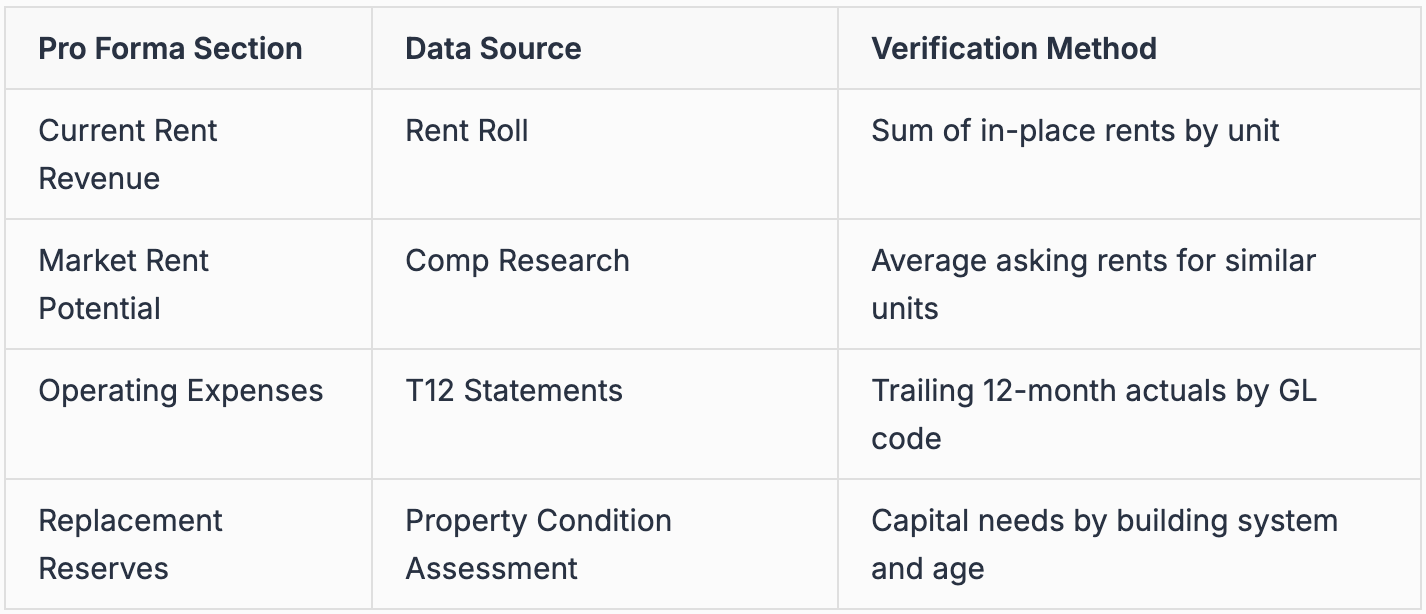

The 10-year pro forma sits at the core of every underwriting package. This projection model demonstrates how the property will perform under base-case assumptions, showing monthly or annual income, expenses, debt service, and cash flow to equity investors.

Essential pro forma components:

Detailed revenue build-up showing unit-level rent growth

Operating expense projections by category with inflation assumptions

Capital expenditure schedule tied to physical needs assessment

Debt service calculations reflecting actual loan terms

Cash-on-cash and IRR returns across the hold period

The pro forma must tie directly to source documents. Every revenue figure should trace back to the rent roll. Every expense assumption should reference T12 historical performance or market benchmarks. Generic models produce clean-looking outputs but fail this verification test.

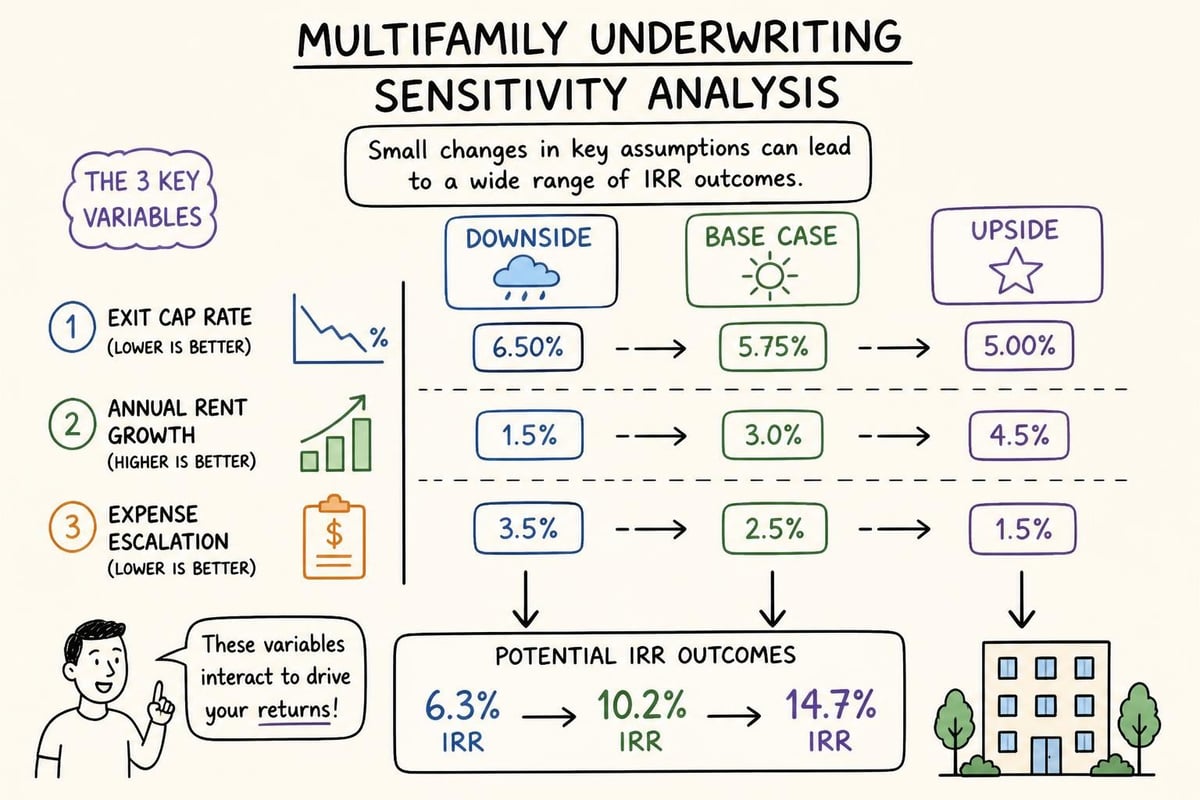

Sensitivity Tables and Scenario Analysis

No underwriting survives contact with reality unchanged. Sensitivity tables demonstrate how returns shift under different exit cap rate, rent growth, and expense escalation scenarios. This analysis identifies which variables drive returns and which assumptions require the highest confidence.

Best practice includes at minimum a three-by-three sensitivity matrix testing base, upside, and downside cases for key variables. More sophisticated teams run Monte Carlo simulations with probability distributions, but these advanced techniques require purpose-built tools rather than basic spreadsheet functionality.

Market Research and Competitive Positioning

The underwriting package must demonstrate thorough market knowledge. This includes submarket supply and demand fundamentals, competitive property positioning, and rental rate justification through comparable analysis.

Market research should answer specific questions rather than provide general market overviews. How does the subject property's rent per square foot compare to directly competitive buildings within a half-mile radius? What amenity packages command rent premiums in this submarket? Which unit types show the tightest supply and strongest absorption?

Source links matter critically here. Statements like "the submarket shows strong fundamentals" mean nothing without supporting data. A proper multifamily underwriting tool automatically links every market assertion to the underlying research report, CoStar data pull, or broker comp sheet.

Risk Identification and Mitigation Strategies

Every deal carries risks that warrant explicit identification and mitigation planning. The underwriting package should flag concentration risks, market timing concerns, execution challenges, and assumption sensitivity.

Common multifamily risk categories:

Lease rollover concentration in specific months

Single tenant representing >10% of revenue

Deferred maintenance exceeding initial capital budget

Submarket supply pipeline potentially oversupplying

Rent growth assumptions exceeding historical performance

Investment committees appreciate honest risk assessment more than optimistic projections. The underwriting tool should surface these flags automatically based on data analysis rather than requiring manual risk writeups that often overlook critical issues.

How Purpose-Built Automation Transforms the Workflow

The difference between generic software and purpose-built back-office automation becomes obvious in production environments. Teams running dozens of deals annually cannot afford the friction introduced by tools designed for general business use. The goal is not another underwriting tool to manage, but an automation layer that can complete repeatable work with source-linked outputs and less analyst supervision.

Automated Document Extraction and Structuring

Modern platforms extract structured data directly from rent rolls and T12 statements regardless of source format. The system recognizes that a PDF from Yardi Voyager has different field layouts than an AppFolio export, but both contain the same underlying information.

This extraction happens autonomously. An analyst uploads the rent roll PDF, and the platform returns a structured dataset with every unit's square footage, current rent, lease start date, lease expiration date, and tenant name. No manual transcription. No formatting cleanup. No reconciliation spreadsheet.

The same capability applies to operating statements. Upload a T12 PDF, and receive categorized income and expense line items mapped to standard general ledger codes. The platform handles embedded formulas, calculates missing subtotals, and flags inconsistencies between reported figures and mathematical results.

Direct Property Management System Integration

The most powerful workflow improvement comes from eliminating manual exports entirely. Rather than requesting rent rolls and operating statements from property management teams, the underwriting platform connects directly to Yardi, RealPage, Entrata, AppFolio, and ResMan.

This integration serves two purposes. First, it ensures data freshness. The underwriting always uses current information rather than potentially outdated PDF snapshots. Second, it enables ongoing monitoring. The same data connections that support initial underwriting power post-acquisition performance tracking.

AI underwriting tools built for real estate understand these property management systems' data structures. The platform knows where tenant information lives within Yardi's database schema, how RealPage structures lease abstracts, and which Entrata tables contain historical financial performance.

Autonomous Multi-Step Task Execution

Generic AI assistants require constant human direction. You ask a question, receive an answer, ask a follow-up, receive another answer. This conversational approach doesn't scale for complex underwriting workflows that require dozens of sequential steps.

A true multifamily underwriting tool accepts high-level instructions and executes complete workflows autonomously. The analyst specifies the property address and underwriting assumptions, then the platform extracts data from all source documents, researches market comparables, builds the financial model, runs sensitivity analyses, and returns a complete underwriting workbook.

This autonomous execution distinguishes purpose-built platforms from general-purpose tools. The difference matters most when teams handle multiple concurrent deals or need rapid turnaround for competitive bid situations. According to industry underwriting standards, speed advantages compound throughout the acquisitions pipeline.

Source-Linked Output and Verification

Every figure in the underwriting package should link directly to its supporting documentation. When the pro forma shows $2.65 per square foot as market rent, clicking that cell should open the comparable property research showing where that figure originated.

This verification capability addresses the fundamental limitation of generic AI models: hallucination. Language models confidently state incorrect information because they optimize for plausible-sounding answers rather than factual accuracy. Real estate underwriting cannot tolerate this uncertainty. Specialized models matter because they are built around the documents, calculations, data structures, and audit requirements that underwriting depends on.

Purpose-built platforms solve this through direct document linking. Every extracted data point maintains its connection to the source PDF page. Every market research figure links to the database query or report that generated it. Investment committees can audit the entire underwriting trail without requesting separate backup documentation.

Continuous Learning and Accuracy Improvement

The most sophisticated multifamily underwriting tool implementations treat data as a compounding asset. Each completed deal adds to the platform's knowledge base, improving future analysis quality and speed.

Portfolio Data Ingestion Enhances Predictions

When a platform processes only individual deals in isolation, it cannot develop meaningful benchmarks. Processing an entire portfolio's historical performance enables pattern recognition that benefits all future underwriting.

The platform learns which expense categories show the strongest correlation with property age. It identifies submarket-specific rent growth patterns. It recognizes how unit mix affects operating expense ratios. This institutional knowledge accumulates silently, improving assumption quality without requiring explicit analyst input.

Teams running hundreds of annual transactions through the same platform achieve accuracy levels impossible with deal-by-deal manual analysis. The AI real estate deal analyzer becomes progressively smarter as data volume increases.

Post-Acquisition Performance Monitoring

Underwriting doesn't end at acquisition. The best teams track how actual performance compares to underwriting projections, identifying which assumptions proved accurate and which require calibration.

This requires ongoing data connections to the same property management systems used for initial underwriting. The platform automatically pulls monthly operating statements, compares actual results to pro forma projections, and flags meaningful variances for asset management review.

These variance reports become the foundation for assumption refinement. When actual rent growth consistently exceeds or falls short of projections, the underwriting model adjusts its baseline assumptions for similar future deals. When specific expense categories show unexpected volatility, the platform widens sensitivity ranges.

Generic Model Limitations

General-purpose AI tools serve valuable functions but cannot replace purpose-built underwriting platforms. Understanding these limitations prevents teams from over-relying on tools designed for different use cases.

Manual Reconciliation Requirements

Language models generate plausible-sounding outputs that require extensive verification. An AI assistant might draft pro forma assumptions, but analysts must manually verify every figure against source documents. This verification often takes longer than building assumptions from scratch.

The reconciliation burden grows with deal complexity. Simple acquisitions with straightforward rent rolls might work adequately with generic tools. Large mixed-use properties with multiple revenue streams, complex expense structures, and varied lease terms overwhelm general-purpose platforms that lack real estate-specific logic.

Output Reliability and Audit Trail Gaps

Investment committees increasingly demand complete audit trails showing underwriting logic and data sources. Generic AI cannot provide this documentation because it doesn't maintain structured connections between inputs, processing steps, and outputs.

When questioned about specific figures, generic tools either cannot explain their derivation or provide generic explanations that don't reference actual source documents. This opacity creates compliance risks and undermines stakeholder confidence in analytical rigor.

Workflow Integration Challenges

Standalone AI assistants require continuous copying and pasting between systems. Extract rent roll data, paste into the AI tool, copy the structured output, paste into Excel, format for analysis, export for the underwriting model. Each handoff introduces error risk and workflow friction.

Purpose-built platforms eliminate these integration gaps by handling the entire workflow within a single environment. Documents upload once. Data extraction, market research, financial modeling, and package creation happen sequentially without manual transfers. The completed underwriting package exports directly to investment committee presentation formats.

Building the Modern Underwriting Stack

Forward-thinking acquisitions teams recognize that competitive advantage increasingly comes from analytical infrastructure rather than individual analyst skill. The firms that close deals fastest with highest accuracy operate fundamentally different technology stacks than those still relying on manual processes.

The foundation starts with document intelligence that handles unstructured inputs. Rent rolls, operating statements, and offering memorandums arrive in inconsistent formats that traditional software cannot process. Modern platforms treat these documents as data sources rather than static files.

Market research integration follows. Rather than maintaining separate subscriptions to multiple data providers and manually reconciling their outputs, the platform should aggregate research from all available sources and present unified comp sets with full sourcing attribution.

Financial modeling sits atop this data infrastructure. When the underlying data extraction and market research happen automatically, analysts spend their time on genuine analysis: evaluating trade-offs, stress-testing assumptions, and crafting investment narratives rather than building spreadsheets.

The workflow concludes with automated package creation. Investment committee memos, presentation decks, and risk summaries generate automatically based on the completed underwriting model. This final automation step ensures consistency across deals and eliminates the rushed formatting work that typically happens hours before IC meetings.

Measuring Tool Performance and ROI

Implementing a new multifamily underwriting tool requires investment in software costs, training time, and workflow adjustment. Sophisticated teams establish clear performance metrics before deployment to measure actual value delivery.

Key performance indicators for underwriting tools:

Average hours from document receipt to completed underwriting package

Error rate in extracted data compared to manual verification

Number of concurrent deals one analyst can handle effectively

Investment committee approval rate for underwriting recommendations

Post-acquisition variance between projected and actual performance

The hours-saved metric captures immediate operational efficiency. Teams that previously required 20-30 hours per underwriting should target 5-10 hours with proper automation. This time compression enables the same team to evaluate more deals or apply saved hours to deeper market research and scenario analysis. The economic case is straightforward: if the system can produce reliable, verifiable work at a fraction of the manual analyst cost, underwriting becomes scalable back-office infrastructure rather than a staffing bottleneck.

Accuracy improvements matter more than speed for many teams. A multifamily underwriting tool that completes analysis in half the time but introduces more errors delivers negative value. Best-in-class platforms achieve both speed and accuracy improvements simultaneously through structured data extraction and source verification.

Portfolio capacity represents the ultimate scaling metric. A five-person acquisitions team might handle 30-40 deals annually with manual processes. The same team equipped with purpose-built tools should evaluate 80-100 deals while maintaining or improving analytical rigor.

Modern multifamily underwriting demands purpose-built automation that addresses the workflow at the data layer, not just the modeling layer. Teams cannot achieve the speed, accuracy, and scalability required for competitive deal execution using disconnected spreadsheets and general-purpose AI assistants. Leni automates underwriting as one back-office workflow within a broader automation architecture: autonomous extraction from rent rolls and property management systems, source-linked market research, verified financial modeling, and ongoing performance monitoring that continuously improves accuracy. See how Leni transforms underwriting from document-heavy manual processing into verifiable back-office automation.

Johanna Gruber

Johanna has spent the last 8 years helping marketing teams connect with audiences through content. Specializing in B2B SaaS and real estate.

Curious About AI?

Join the largest AI community for real estate online. Get bite-sized, real-world use case videos, plus practical tips and proven strategies from top industry experts on adopting AI effectively.

MEET LENI

AI SuperAgent Purpose Built for Investors and Operators.

Experience how professionals and teams in your domain are getting the edge using AI.