What is the Equal Credit Opportunity Act (ECOA) as it relates to Real Estate?

666.webp&w=1920&q=75)

Learn how the Equal Credit Opportunity Act (ECOA) impacts real estate by ensuring equal access to mortgage loans and financing. Read on! In simple terms, the Equal Credit Opportunity Act is a federal fair lending law that helps make sure mortgage applicants and other borrowers are evaluated on legitimate credit factors rather than protected personal characteristics. In real estate, that makes ECOA one of the most important legal protections governing access to home loans, refinancing, and other property-related credit.

The Equal Credit Opportunity Act (ECOA) is a federal law designed to ensure that all consumers are given an equal chance to obtain credit, including mortgage loans and other forms of real estate financing. Enacted in 1974 and implemented through Regulation B, the ECOA is enforced primarily by the Consumer Financial Protection Bureau (CFPB). It plays a crucial role in the real estate industry by prohibiting lenders and creditors from discriminating against borrowers on the basis of certain protected characteristics. When people think about discrimination in real estate, they often think first about housing access. But financing access matters just as much. A borrower who cannot access fair mortgage credit may be locked out of buying, refinancing, or investing in property even before a housing transaction can move forward. That is why ECOA matters so much in the real estate context.

Below are the key points to understand about the ECOA as it relates to real estate:

Prohibited Grounds for Discrimination

Under the Equal Credit Opportunity Act (ECOA), creditors including mortgage lenders are strictly prohibited from discriminating against applicants based on any of the following factors:

Race

Color

Religion

National origin

Sex

Marital status

Age (as long as the applicant is legally able to enter into a contract)

Receipt of income from public assistance programs

Exercising any rights under the Consumer Credit Protection Act

This matters because ECOA is not limited to obvious denials. It can also apply when similarly qualified borrowers are offered different loan terms, face different documentation standards, or are evaluated through inconsistent underwriting practices.

.webp)

Scope and Coverage

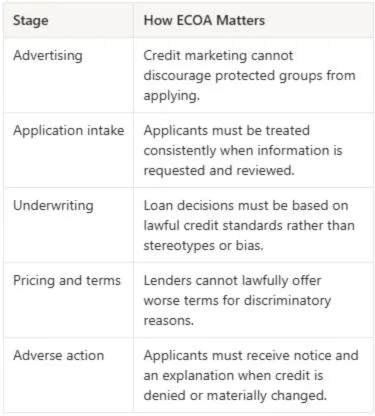

The Equal Credit Opportunity Act (ECOA) covers every stage of a credit transaction ranging from advertising and application to underwriting and loan closing. In the context of real estate, this means lenders must treat all mortgage applicants equally, regardless of their protected characteristics. Discriminatory practices such as offering unequal terms, applying different standards, or denying credit based on bias or stereotypes are strictly prohibited.

Where ECOA Applies in a Real Estate Credit Transaction

Notifications and Reasons for Denial

When a lender denies a mortgage application or takes adverse action such as approving a loan with less favorable terms the borrower has the right to be informed of the reason. Under the ECOA, creditors are required to either provide specific reasons for the denial or notify the applicant of their right to request those reasons within a designated time period. This requirement promotes transparency and allows consumers to better understand and address potential credit issues.

This is one of ECOA’s most practical protections. Without a notice requirement, borrowers could be left with vague denials and no clear understanding of what affected the decision. By requiring transparency, ECOA gives applicants a better chance to correct legitimate credit issues or identify whether unfair treatment may have occurred.

Also Read: How Strategic Rental Asset Management Yields the Biggest Returns

Interaction with Other Laws

The ECOA works alongside other key consumer protection laws, such as the Fair Housing Act (FHA), which addresses discrimination in housing, and the Truth in Lending Act (TILA), which ensures transparency in credit terms. Together, these laws provide comprehensive safeguards against discriminatory and deceptive practices in home financing.

A useful way to think about the distinction is this: ECOA focuses on fair access to credit, the Fair Housing Act focuses on discrimination in housing-related activities, and TILA focuses on clear disclosure of loan terms and borrowing costs. In real estate transactions, these protections often work together rather than separately.

Enforcement and Remedies

Violations of the ECOA can result in civil penalties for lenders. Consumers who suspect discrimination have the right to file a complaint with the Consumer Financial Protection Bureau (CFPB) or pursue legal action. Available remedies may include compensation for actual damages, punitive damages, and coverage of legal costs.

For lenders, brokers, and other real estate finance professionals, this means fair lending compliance is not just a legal formality. It is an operational requirement that affects policies, training, documentation, and underwriting consistency. Even subtle differences in treatment can create meaningful compliance risk.

By fostering a fair lending environment, the Equal Credit Opportunity Act helps ensure that consumers have equitable access to mortgage credit and other real estate financing opportunities, regardless of their background or personal characteristics.

_(1).webp)

Why ECOA Matters in Real Estate

It protects mortgage access: Buyers and borrowers should be judged on creditworthiness, not protected traits.

It improves transparency: Adverse action notice rules help borrowers understand denials and less favorable terms.

It supports fair lending compliance: Real estate finance participants need consistent procedures across the credit process.

It works as part of a broader legal framework: ECOA strengthens fair access to financing alongside housing and disclosure laws.

Frequently Asked Questions

1. Does ECOA apply only to mortgage lenders?ECOA applies more broadly to creditors in credit transactions, but in real estate it is especially important for mortgage lending, refinancing, and other property-related financing decisions.

2. Can a lender ask about marital status or age?There are limited situations where certain information may be requested for lawful reasons, but lenders cannot use protected characteristics in a discriminatory way when making credit decisions.

3. Does ECOA only cover outright denials?No. ECOA can also apply when a borrower receives less favorable terms, faces inconsistent underwriting treatment, or is discouraged from applying for credit.

4. Why is ECOA important to real estate professionals who are not lenders?Because financing is central to many real estate transactions. Agents, brokers, housing professionals, and investors all benefit from understanding the fair lending rules that affect borrowers and deals.

5. What is the key takeaway for borrowers?ECOA helps ensure that access to real estate credit is based on legitimate financial criteria rather than discrimination, and it gives applicants important rights when credit is denied or changed.

Final Takeaway

The Equal Credit Opportunity Act matters because fair access to credit shapes who gets to buy, refinance, and invest in real estate in the first place. Its importance is not limited to stopping obvious discrimination. It also pushes the lending process toward greater consistency, transparency, and accountability.

That remains true even as the industry adopts more technology. Tools like Leni can help teams review information, organize analysis, and move faster, but the underlying standard does not change: better processes only matter if access to credit remains fair. That is the real point of ECOA, and why it still matters.

AI in Real Estate Community

Connect with asset managers, operators, and investors navigating AI adoption in real estate.

Latest Help Articles

Learn about how AI is changing the investment world with in-depth research and industry voices.

MEET LENI

Purpose Built Agentic Platform for Investors

Designed for people who want to do serious work using AI.

We Work with Leaders Shaping the Industry

From automating portfolio reporting to market research, learn how leaders are integrating AI in their businesses.