How to Analyze an Investment Property: A Complete Guide

.webp&w=1920&q=75)

How to Analyze an Investment Property: A Complete Guide

Most acquisitions teams follow the same inefficient playbook when evaluating deals: download documents, manually extract data into spreadsheets, build models from scratch, hunt for comparable properties that may not tie out, and repeat this process for every opportunity. This approach consumes hours or days per property and introduces errors that compound through the underwriting process. Learning how to analyze an investment property correctly means understanding both the fundamental metrics and the workflow that delivers accurate, defensible results. This guide walks through the complete analysis process, from initial data gathering to final investment recommendation, with a focus on the inputs, outputs, and tools that separate thorough analysis from guesswork.

Gather Essential Property Documents and Data

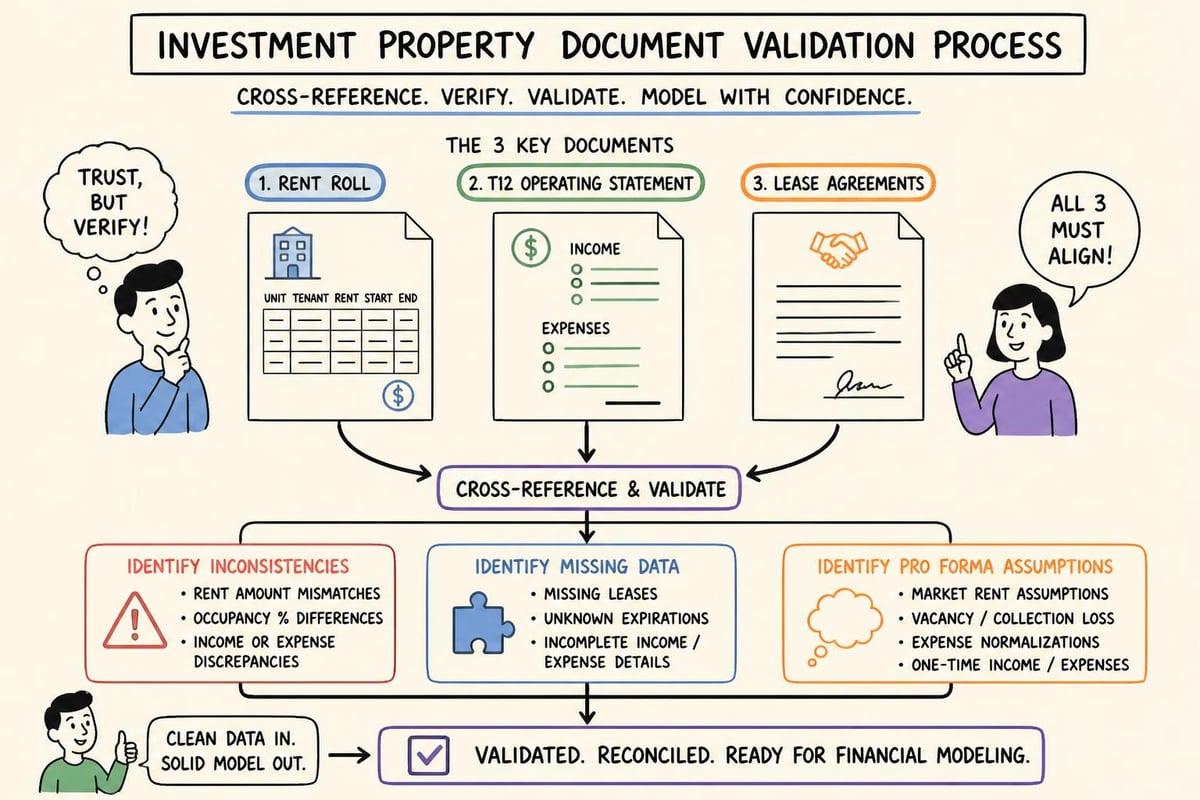

Before calculating a single metric, you need complete and accurate source documents. The quality of your analysis depends entirely on the quality of your inputs.

Required Documents for Commercial Property Analysis

Every thorough property analysis starts with three foundational document types:

Rent rolls showing current tenant roster, lease terms, square footage, rental rates, and expiration dates

Trailing twelve-month operating statements (T12s) detailing actual income and expenses over the past year

Offering memorandums (OMs) containing property details, market positioning, and seller projections

Additional documents strengthen your analysis:

Historical operating statements (ideally three to five years)

Current lease agreements for major tenants

Capital expenditure reports and deferred maintenance assessments

Property condition reports and environmental assessments

Local market reports and comparable sales data

The document extraction process traditionally requires manual data entry, consuming hours and introducing transcription errors. Modern platforms automate this step, pulling structured data directly from PDFs and connecting it to your financial models.

Validate Data Accuracy Before Analysis

Raw documents often contain inconsistencies. Rent rolls may not match lease files. Operating statements may categorize expenses differently year over year. Seller proformas frequently present optimistic assumptions.

Create a validation checklist:

Cross-reference rent roll totals against actual lease agreements

Compare T12 income against bank statements or audited financials when available

Identify unusual expense items or categories that seem understated

Flag tenants approaching lease expiration within 12 months

Note any revenue or expense items marked as "pro forma" rather than actual

This verification step prevents downstream errors that invalidate your entire analysis. When accuracy matters, almost right is wrong.

Calculate Core Financial Performance Metrics

Understanding how to analyze an investment property requires mastering four foundational metrics that reveal different aspects of property performance and investment return.

Net Operating Income (NOI)

Net Operating Income represents the property's annual income after operating expenses but before debt service and capital expenditures. This metric serves as the foundation for most other calculations.

NOI Formula: Gross Potential Rent + Other Income - Vacancy Loss - Operating Expenses = NOI

Operating expenses include:

Property management fees (typically 3% to 5% of effective gross income)

Property taxes and insurance

Utilities paid by landlord

Repairs and maintenance

Administrative costs

Marketing and leasing commissions

Operating expenses exclude:

Mortgage payments (debt service)

Capital improvements

Depreciation and amortization

Income taxes

For a multifamily property with $500,000 in effective gross income and $200,000 in operating expenses, the NOI equals $300,000. Increasing NOI directly impacts property value and return metrics.

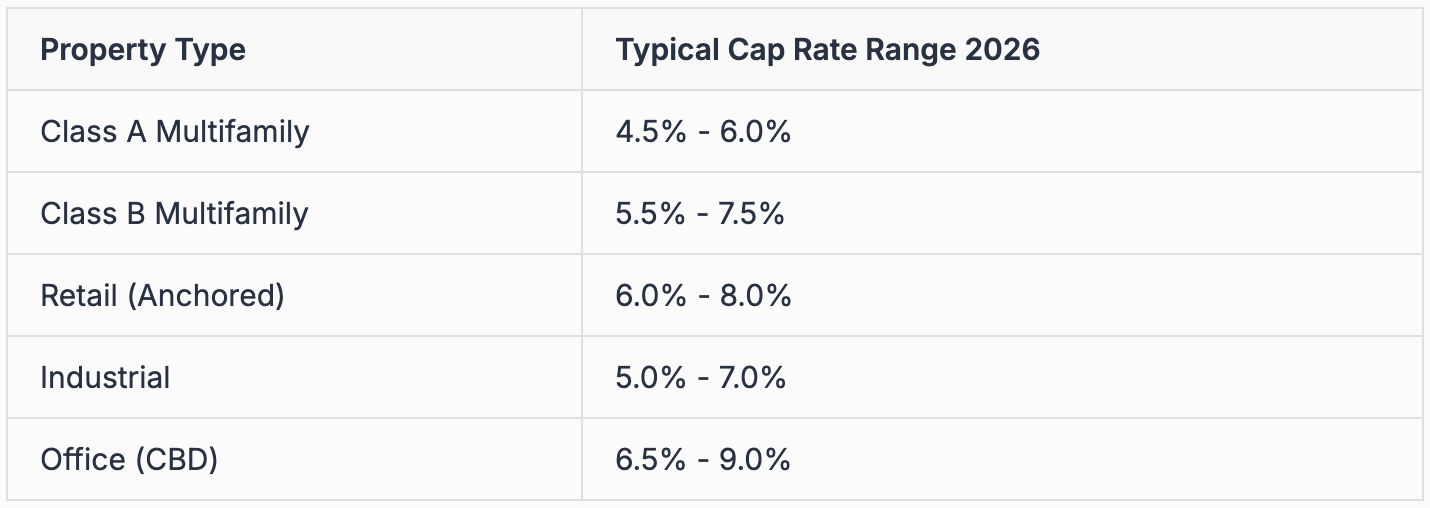

Capitalization Rate (Cap Rate)

The capitalization rate measures the relationship between a property's NOI and its purchase price, providing a snapshot of expected annual return independent of financing.

Cap Rate Formula: (Net Operating Income ÷ Purchase Price) × 100 = Cap Rate %

A property generating $300,000 NOI with an $4,000,000 purchase price delivers a 7.5% cap rate. This metric enables quick comparison across properties and markets.

Cap rates vary significantly by property type, location, and market conditions:

Lower cap rates indicate lower perceived risk and higher property values. Market research reveals local cap rate trends essential for competitive bidding.

Cash-on-Cash Return

While cap rate ignores financing, cash-on-cash return measures actual cash return on invested equity, accounting for mortgage payments.

Cash-on-Cash Formula: (Annual Pre-Tax Cash Flow ÷ Total Cash Invested) × 100 = Cash-on-Cash Return %

Using our previous example with 70% loan-to-value financing:

Purchase price: $4,000,000

Down payment: $1,200,000

Loan amount: $2,800,000 at 6.5% interest

Annual debt service: $224,000

NOI: $300,000

Annual cash flow: $76,000 ($300,000 NOI - $224,000 debt service)

Cash-on-cash return: 6.3% ($76,000 ÷ $1,200,000)

This metric reveals how leverage impacts actual returns to equity investors.

Debt Service Coverage Ratio (DSCR)

Lenders require properties to generate sufficient income to cover mortgage payments with a safety margin. The DSCR calculation determines whether a property qualifies for financing.

DSCR Formula: Net Operating Income ÷ Annual Debt Service = DSCR

For our example property: $300,000 NOI ÷ $224,000 debt service = 1.34 DSCR

Most commercial lenders require minimum DSCR between 1.20 and 1.35, depending on property type and market conditions. Higher ratios indicate stronger ability to weather income disruptions or expense increases.

Build a Comprehensive Pro Forma Model

Static metrics provide snapshots, but investment decisions require projections. A proper pro forma model forecasts property performance over your intended holding period, typically five to ten years.

Essential Pro Forma Components

Your model must project these elements annually:

Gross potential rent with market rent growth assumptions

Vacancy and credit loss based on historical performance and market conditions

Operating expense growth typically 2% to 3% annually

Capital expenditures for major systems and tenant improvements

Debt service including principal and interest payments

Exit assumptions including terminal cap rate and selling costs

The Redfin guide on evaluating investment properties emphasizes the importance of conservative assumptions in pro forma modeling.

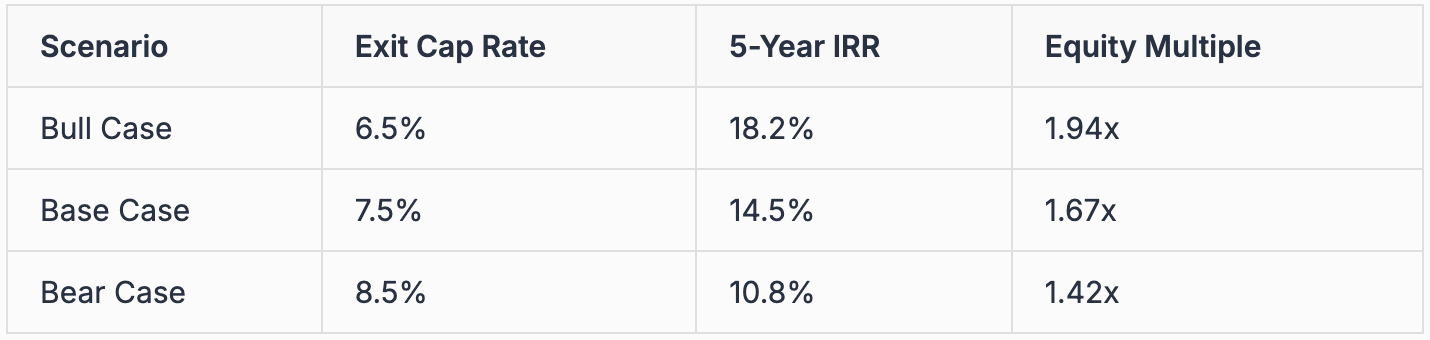

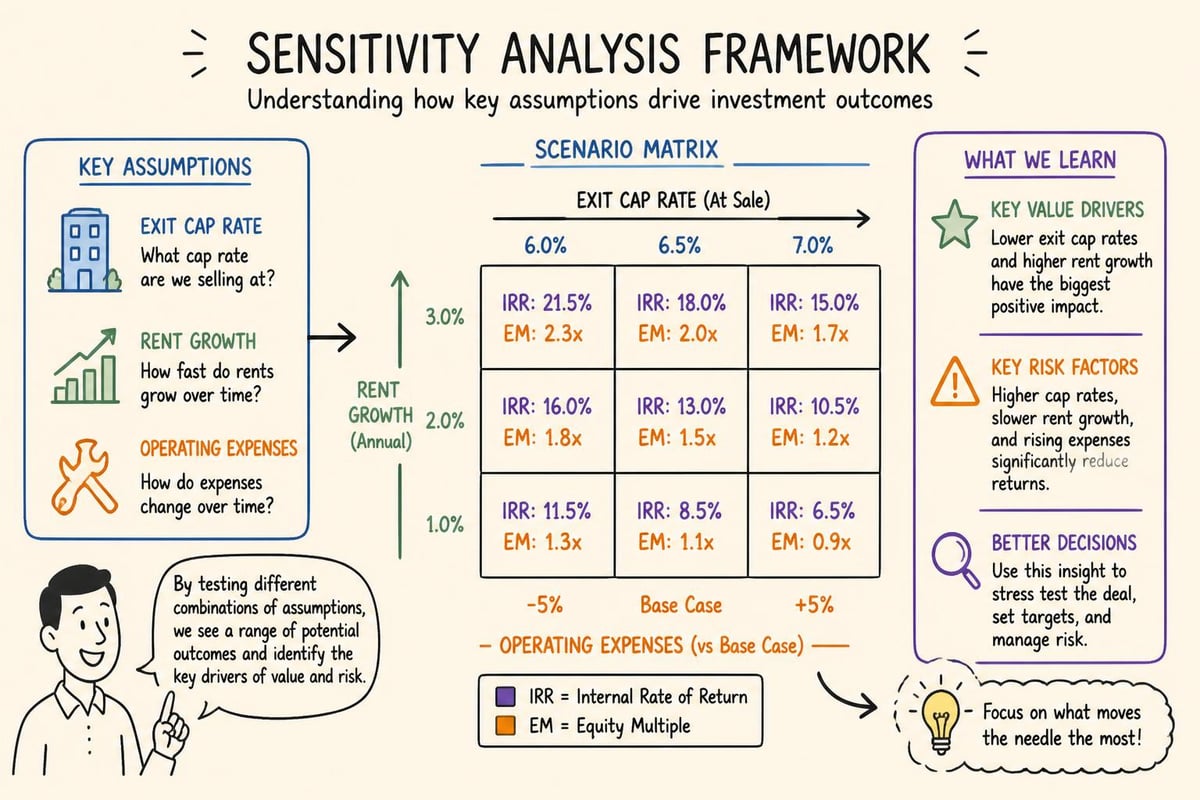

Sensitivity Analysis for Risk Assessment

Single-point forecasts ignore uncertainty. Professional analysis includes sensitivity tables showing how returns change across varying scenarios:

Test sensitivity across:

Exit cap rate (±50 to 100 basis points)

Rent growth (±1% annually)

Vacancy rate (±5% absolute)

Operating expense growth (±1% annually)

This analysis reveals which assumptions drive returns and where risks concentrate. According to Real Estate Insights, understanding these metrics through scenario planning separates sophisticated investors from those who rely on seller assumptions.

Conduct Market and Comparable Property Research

No property exists in isolation. Understanding how to analyze an investment property requires contextualizing it within its competitive market.

Identify True Comparable Properties

Effective comparable analysis matches properties across multiple dimensions:

Property type and class (don't compare Class A to Class C)

Location and submarket (walkability, employment centers, demographics)

Unit mix and amenities for multifamily

Tenant quality and lease terms for commercial

Transaction timing (sales within past 6 to 12 months)

Many investors rely on publicly available comparable sales, but these often lack crucial details like actual NOI, deferred maintenance, or special financing terms. The PropLab approach to analyzing real estate deals emphasizes verified comparables with complete financial data.

Market Trend Analysis

Beyond static comparables, analyze directional trends:

Rent growth trajectories over the past 36 months

Absorption rates and new supply pipeline

Employment and population growth in the submarket

Transaction volume and investor appetite

Tenant retention rates and lease renewal terms

Modern commercial real estate analytics platforms aggregate this data from multiple sources, providing source-linked verification for every data point.

Identify and Quantify Investment Risks

Every property carries risks that impact projected returns. Systematic risk assessment prevents surprises post-acquisition.

Property-Level Risks

Physical and operational risks specific to the asset:

Deferred maintenance requiring immediate capital deployment

Environmental issues like asbestos or soil contamination

Tenant concentration with single tenants representing over 20% of income

Near-term lease rollover requiring re-tenanting costs

Functional obsolescence reducing competitive position

Market and External Risks

Factors beyond property-level control:

Economic sensitivity to local employment changes

New competing supply under construction or planned

Regulatory changes affecting zoning or rent control

Interest rate exposure on floating-rate debt or refinancing

Exit market liquidity for the property type

Create a risk matrix scoring each factor on probability and impact. High-probability, high-impact risks require mitigation strategies or deal termination.

Evaluate Value-Add and Repositioning Opportunities

The best deals often involve properties trading below replacement cost with clear paths to operational improvement. Deal Run's analysis approach emphasizes identifying these opportunities systematically.

Common Value-Add Strategies

Revenue enhancement opportunities:

Below-market rents requiring systematic increases to market

Underutilized space convertible to income-producing areas

Fee income from parking, storage, or amenity charges

Service add-ons like high-speed internet or furnished units

Expense reduction opportunities:

Management inefficiencies correctable through better systems

Utility expense reduction through conservation measures

Insurance and tax appeal opportunities

Vendor contract renegotiation

Quantifying Value Creation

Calculate the impact of improvements on property value:

If implementing value-add strategies increases NOI by $50,000 annually, and the market cap rate is 7.0%, the value creation equals approximately $714,000 ($50,000 ÷ 0.07).

Factor implementation costs and timeline into your analysis:

Capital required for physical improvements

Lost income during renovation or lease-up

Professional fees for planning and execution

Financing costs for value-add capital

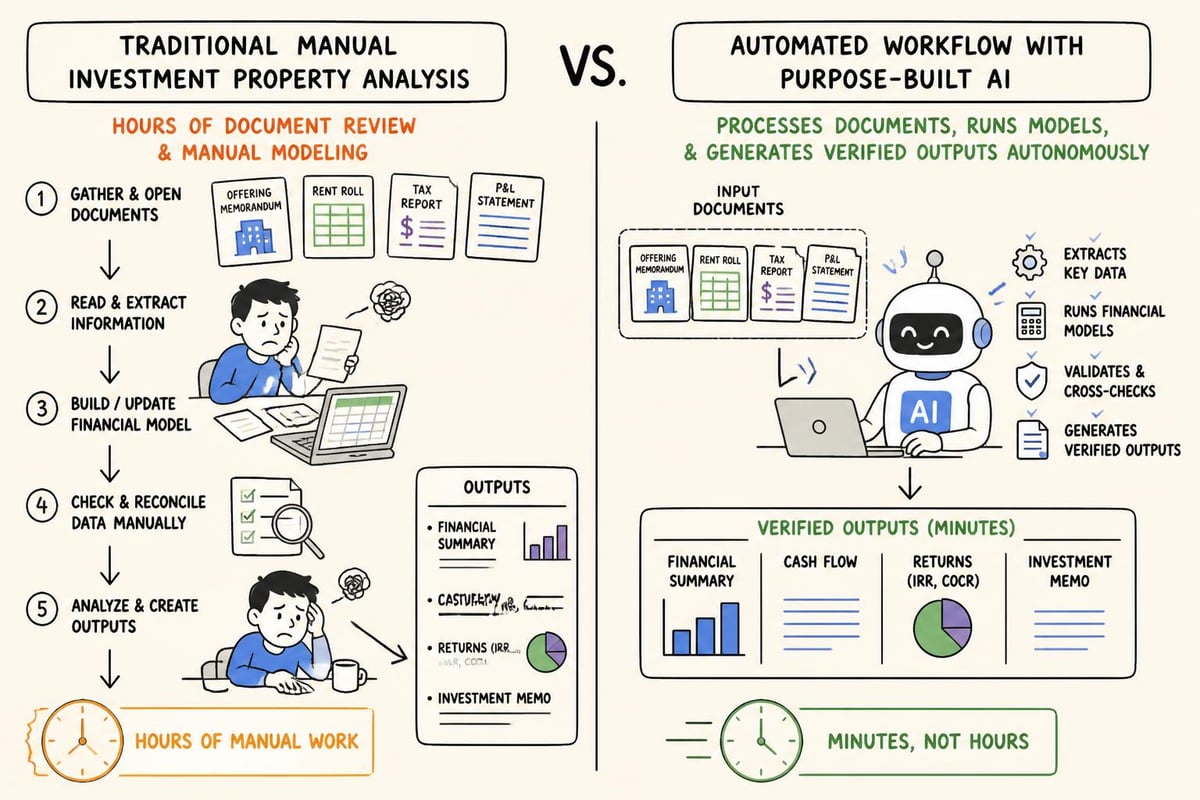

Automate Analysis Workflow with Purpose-Built Tools

Traditional analysis requires assembling data from multiple sources, manually building financial models, chasing down comparable properties, and hoping calculations tie out correctly. This process consumes 15 to 60 minutes for simple deals and days for complex portfolios.

The Limitations of Generic AI Tools

ChatGPT, Gemini, and similar general-purpose AI platforms offer brainstorming capabilities but fall short for investment analysis:

They require constant prompting and supervision

Outputs often contain calculation errors or unsourced assumptions

They cannot connect directly to property management systems

They lack verification links to source documents

They produce inconsistent results across similar queries

When evaluating multimillion-dollar investments, "almost right" equals wrong. The investment property analysis software landscape has evolved to address these limitations.

Purpose-Built Analysis Platforms

Leni represents a different approach: an AI analyst platform specifically designed for commercial real estate that runs complete analysis workflows autonomously. Rather than answering individual questions, it handles multi-step tasks from document upload through finished deliverables.

Key workflow capabilities:

Upload rent rolls, T12s, and offering memorandums in any format

Automatic data extraction with source linking for verification

Financial modeling and underwriting with sensitivity analysis

Market comparable research with verifiable source links

Investment committee memo and presentation creation

Direct integration with Yardi, RealPage, and Entrata systems

The platform runs autonomously for 15 to 60 minutes per property, returning completed analysis you can verify and defend. SOC 2 Type 2 certification ensures data security for institutional workflows.

Accuracy Standards That Matter

Generic AI platforms often produce plausible-sounding outputs that don't withstand scrutiny. Leni achieved 98% accuracy on BullshitBench (ranked first among tested platforms), demonstrating consistent reliability on factual analysis tasks.

More importantly, every output includes direct links to source documents, enabling verification of every assumption and calculation. This transparency matters when presenting to investment committees or lenders who demand defensible analysis.

Structure Investment Committee Recommendations

Analysis exists to drive decisions. The final deliverable must communicate findings clearly to stakeholders with varying technical backgrounds.

Essential IC Memo Components

Investment committee memorandums should include:

Executive summary with deal thesis and recommendation

Property overview including location, specifications, and tenant details

Market analysis with comparable sales and trend data

Financial projections showing base case and sensitivity scenarios

Risk assessment identifying key concerns and mitigation strategies

Value creation plan detailing operational improvements

Investment metrics summary with returns across scenarios

Recommendation with specific conditions or contingencies

The investment memo creation process traditionally requires assembling insights from multiple analyses into coherent narratives, a time-consuming task that delays decision-making.

Visual Communication for Complex Analysis

Numbers alone rarely persuade. Effective presentations combine data with clear visual communication:

Waterfall charts showing sources and uses of capital

Sensitivity tables highlighting return ranges

Market maps positioning the property against competitors

Timeline graphics illustrating value-add implementation

Comparison matrices evaluating this opportunity against alternatives

Professional presentations reflect analytical rigor and build confidence in recommendations.

Execute Due Diligence with Systematic Verification

Preliminary analysis identifies whether to proceed with an offer. Due diligence confirms whether to close.

Due Diligence Checklist by Category

Financial verification:

Audit actual rent collections against reported figures

Review three years of tax returns and audited financials

Verify tenant security deposits held in escrow

Confirm all utility accounts and payment history

Review capital expenditure records for deferred items

Legal and regulatory:

Title review identifying encumbrances or easements

Zoning compliance and any non-conforming uses

Review all leases for unusual provisions or tenant rights

Verify property tax assessments and pending appeals

Environmental Phase I (and Phase II if triggered)

Physical inspection:

Professional property condition assessment

Major systems review (HVAC, roofing, electrical, plumbing)

Life safety systems compliance (fire suppression, egress)

ADA compliance for common areas

Seismic or flood risk assessment where applicable

According to Lineage's evaluation framework, systematic due diligence prevents costly surprises that undermine projected returns.

Document Your Findings and Negotiations

Due diligence almost always reveals discrepancies requiring seller resolution:

Deferred maintenance requiring credits or escrow holdbacks

Rent roll discrepancies requiring lease file verification

Environmental concerns requiring remediation or price adjustment

Legal issues requiring seller cure before closing

Document all findings in detail. Quantify financial impacts. Present clear resolution requirements with supporting evidence. Strong documentation enables effective negotiation and protects against post-closing disputes.

Knowing how to analyze an investment property separates successful acquisitions from expensive mistakes, but the traditional workflow wastes time and introduces errors that compound throughout underwriting. Leni eliminates these inefficiencies by running the complete analysis workflow autonomously, from document extraction through financial modeling, market research, and IC memo creation, all with verifiable source links you can defend. Upload your next deal's documents and let Leni handle the analytical heavy lifting while you focus on sourcing and negotiating.

Johanna Gruber

Johanna has spent the last 8 years helping marketing teams connect with audiences through content. Specializing in B2B SaaS and real estate.

Curious About AI?

Join the largest AI community for real estate online. Get bite-sized, real-world use case videos, plus practical tips and proven strategies from top industry experts on adopting AI effectively.

MEET LENI

AI SuperAgent Purpose Built for Investors and Operators.

Experience how professionals and teams in your domain are getting the edge using AI.