Multifamily Underwriting Software: Complete Guide 2026

Multifamily Underwriting Software: Complete Guide 2026

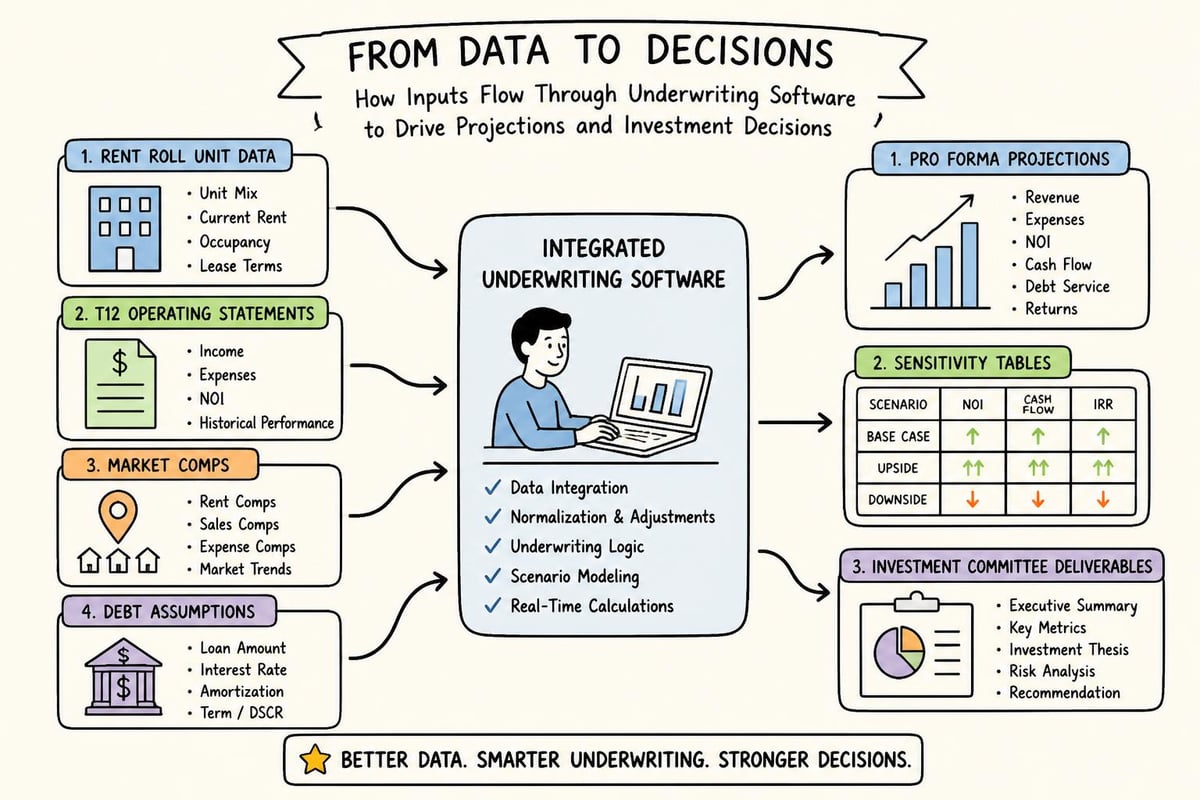

Multifamily acquisitions teams process thousands of data points during underwriting: rent rolls with hundreds of units, trailing twelve-month operating statements, market comps across submarket boundaries, debt assumption scenarios, and sensitivity tables testing cap rate compression. The traditional approach involves Excel workbooks, disconnected market research tabs, manual lease abstraction, and siloed memo drafting. Modern multifamily underwriting software transforms this fragmented process into integrated workflows that connect property-level analysis to portfolio-wide reporting, enabling faster deal evaluation without sacrificing accuracy or audit trails.

Understanding Multifamily Underwriting Software Requirements

Underwriting multifamily assets demands specialized functionality that general-purpose financial tools cannot address. Your software must ingest rent rolls and reconcile unit-level data against trailing twelve statements, calculate stabilized net operating income under multiple scenarios, and generate sensitivity matrices testing various exit cap rates and hold periods.

The core workflow begins with document extraction. Rent rolls arrive as PDFs with inconsistent formatting, confidential information memorandums contain critical assumptions buried in footnotes, and operating statements require normalization across different ownership periods. Effective multifamily underwriting software automates this extraction step, converting unstructured documents into structured datasets ready for financial modeling.

Critical Data Points Your Platform Must Handle

Your underwriting system processes both current performance metrics and forward-looking assumptions. Each category requires different validation logic and calculation methodologies.

Current Performance Inputs:

Unit-level rent rolls with lease expiration dates

Trailing twelve-month income and expense statements

Historical occupancy trends and leasing velocity

Capital expenditure reserves and deferred maintenance

Property tax assessments and utility consumption

Forward-Looking Assumptions:

Market rent growth projections by unit type

Expense escalation factors for controllable versus non-controllable items

Renovation budgets and stabilization timelines

Financing terms including loan-to-value ratios and debt service coverage requirements

Exit assumptions with terminal cap rate ranges

The software must link these inputs to outputs like internal rate of return, equity multiple, and cash-on-cash returns while maintaining complete transparency into every calculation step. Understanding commercial real estate analytics fundamentals helps teams evaluate whether platforms provide the necessary depth for institutional-grade analysis.

Evaluating Software Architecture and Integration Capabilities

The technical architecture underlying your multifamily underwriting software determines its scalability and reliability. Cloud-native platforms offer continuous access for distributed teams, while legacy desktop applications create version control nightmares when multiple analysts work on the same deal.

Integration with property management systems represents a critical evaluation criterion. Direct connections to Yardi, RealPage, and Entrata eliminate manual data entry and reduce transcription errors. When your platform pulls actuals directly from the PMS, you build underwriting models on verified data rather than assumptions extracted from seller-provided documents.

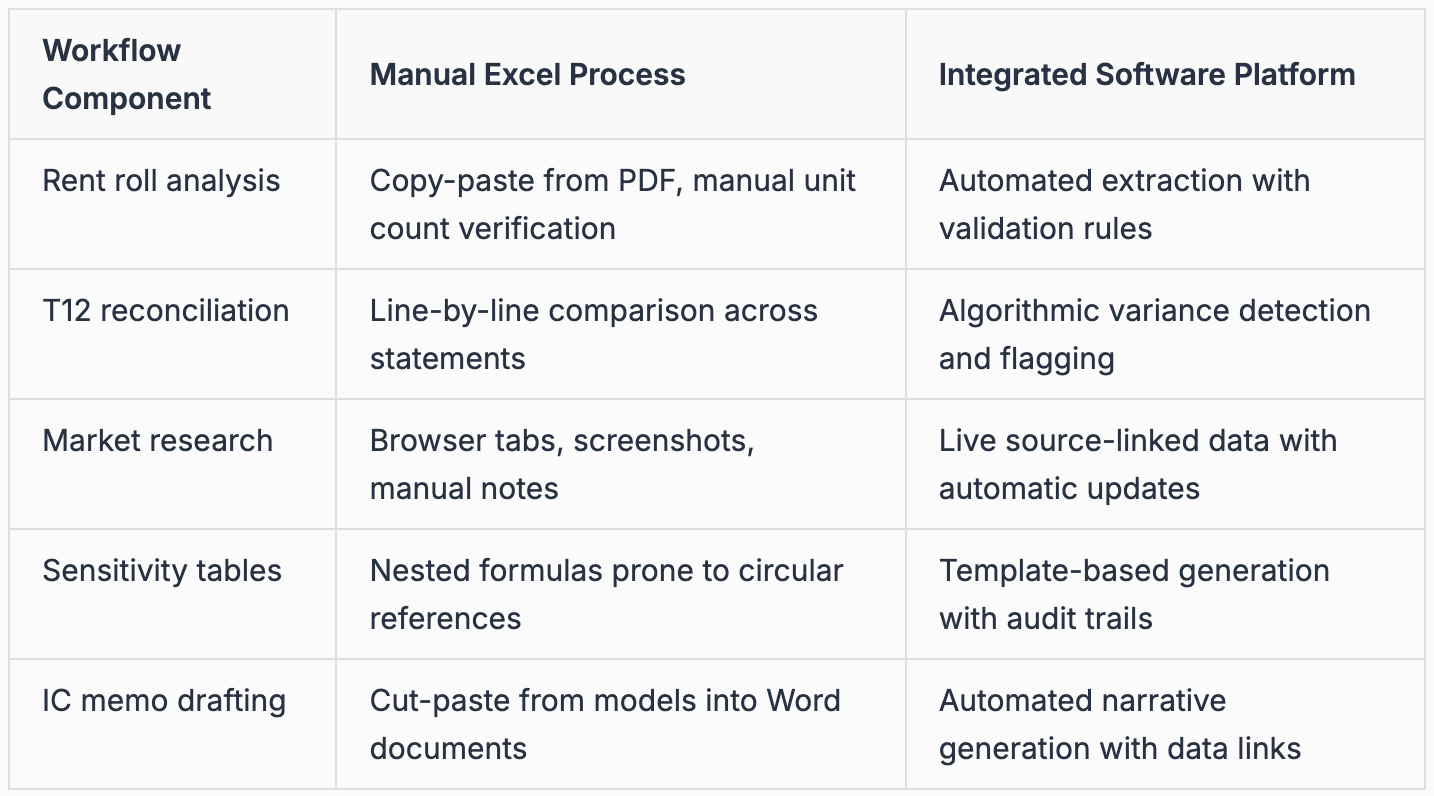

Comparing Manual Versus Automated Workflows

Traditional workflows force analysts to toggle between applications, increasing cognitive load and error probability. Advanced AI tools for business analysts eliminate context switching by keeping all underwriting components within a unified interface.

Building Standardized Financial Models

Consistency across deals enables meaningful portfolio-level analysis. Your multifamily underwriting software should enforce standardized assumptions while allowing property-specific adjustments. This balance ensures apples-to-apples comparison during portfolio reviews without sacrificing deal-specific nuance.

Start with a template structure that captures your organization's investment criteria. Define required sensitivity analyses, establish base case assumptions for market rent growth and expense escalation, and specify hold period parameters. The software should apply these defaults while flagging deviations that exceed predetermined thresholds.

Key Financial Model Components

Income Projections:

Calculate current in-place rent versus market rent by unit type

Apply vacancy and credit loss assumptions based on submarket performance

Project rental growth using compound annual growth rates adjusted for lease-up periods

Add ancillary income from parking, storage, and utility reimbursements

Model rental premiums from value-add renovations with specific completion timelines

Operating Expense Forecasting:

The software must distinguish between controllable and non-controllable expenses. Property taxes follow assessment cycles and appeal outcomes, insurance premiums reflect carrier market conditions, and utilities depend on consumption patterns. Controllable expenses like payroll and maintenance respond to operational decisions.

Build expense forecasts using base year actuals adjusted for inflation factors specific to each category. Property management fees typically calculate as a percentage of effective gross income, while repair budgets may require unit-level allocations based on age and condition.

Capital Planning and Reserve Analysis:

Separate immediate capital needs from long-term reserves. The underwriting model should track both initial acquisition renovations and ongoing replacement reserves. Strategies to increase NOI often involve upfront capital investment that depresses cash flow during early hold years before delivering enhanced returns at stabilization.

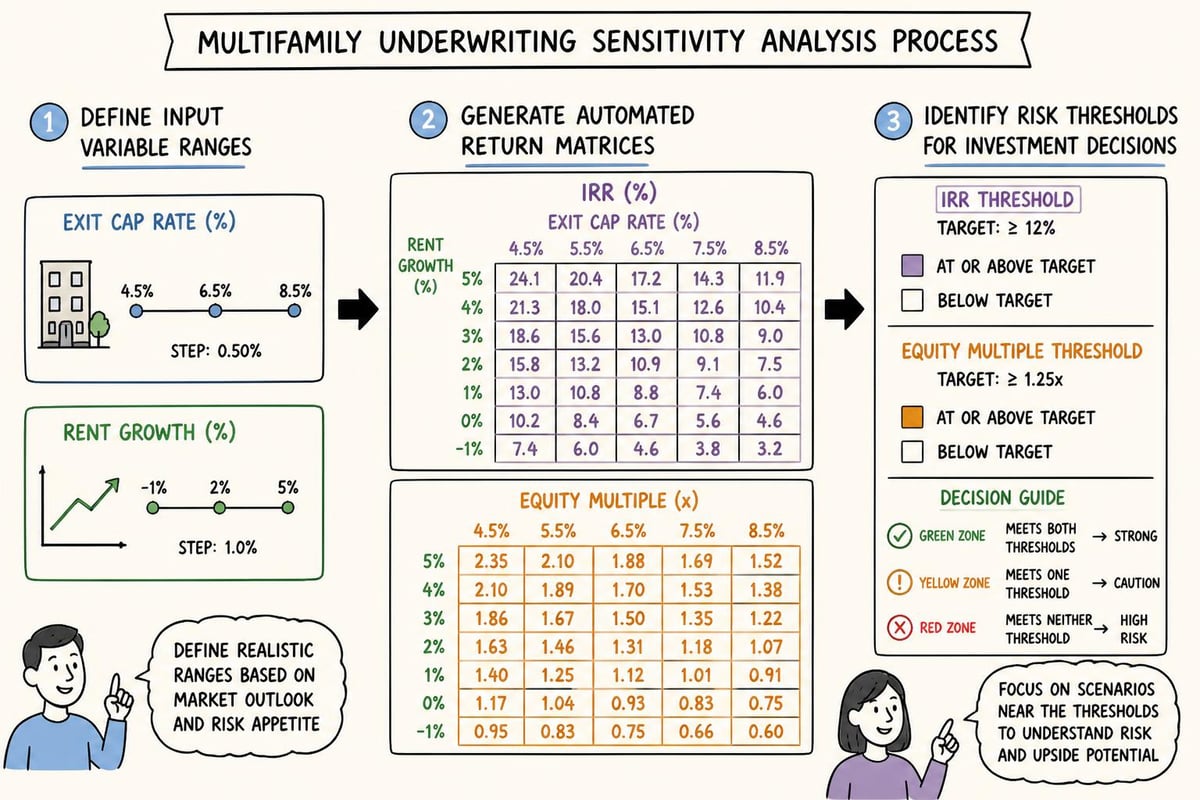

Executing Sensitivity and Scenario Analysis

Single-point estimates obscure investment risk. Robust multifamily underwriting software generates sensitivity tables testing how returns respond to assumption changes. Build matrices showing IRR variation across exit cap rate and hold period combinations, or test how rent growth and expense assumptions interact.

The platform should enable rapid scenario comparison. Create a base case reflecting your investment committee's standard assumptions, then develop downside scenarios testing stressed market conditions and upside scenarios incorporating accelerated lease-up or premium exit pricing.

Structuring Sensitivity Tables

Effective sensitivity analysis requires thoughtful axis selection. Common multifamily sensitivity dimensions include:

Exit cap rate ranges (typically ±50 to 100 basis points from base case)

Rent growth assumptions (testing market, submarket, and property-specific drivers)

Renovation cost overruns and timeline extensions

Interest rate impacts on debt service and refinancing scenarios

Disposition timing windows aligned with market cycle positioning

Your software should calculate these sensitivities automatically when you adjust input ranges. Real-time recalculation helps acquisitions teams understand risk boundaries during live investment committee meetings. Common multifamily underwriting mistakes often stem from insufficient sensitivity testing around key value drivers.

Conducting Market Research and Comparable Analysis

Investment decisions require market context. Your multifamily underwriting software should integrate market research directly into the underwriting workflow rather than forcing analysts to maintain separate research files. Link property-level assumptions to submarket rental surveys, comparable sales transactions, and demographic trends.

Effective comp analysis goes beyond simple averages. Weight recent transactions more heavily, adjust for property quality differences, and account for location premiums. The software should enable side-by-side comparison showing how your subject property's metrics stack against recent trades on a per-unit and per-square-foot basis.

Building a Defensible Comps Database

Transaction Comps:

Document sale price per unit, cap rate at sale, year built, unit count, and submarket location for every comparable transaction. Filter by recency, with most investment committees preferring comps from the trailing twelve months. Older transactions require adjustment factors reflecting market appreciation.

Rental Comps:

Track asking rents by unit type across competing properties within your subject's submarket. Document concessions, amenity packages, and renovation status. Calculate effective rents after concession adjustments to avoid overstating market rent potential.

Live source-linked market research capabilities ensure your underwriting reflects current market conditions rather than stale data from initial property tours. When market fundamentals shift during due diligence, integrated platforms update assumptions automatically rather than requiring manual model revisions.

Generating Investment Committee Deliverables

Investment committee presentations require synthesizing quantitative analysis into compelling narratives. Modern multifamily underwriting software automates IC memo creation, pulling key metrics from financial models and market research into standardized report templates.

The software should generate executive summaries highlighting investment thesis, risk factors, and return metrics. Include property-level details covering location analysis, competitive positioning, and operational value-add strategies. Financial sections present pro forma projections, sensitivity matrices, and returns waterfall allocations.

Structuring Effective IC Memos

Executive Summary Section:

Investment highlights and thesis statement

Purchase price and capitalization structure

Projected returns across base and sensitivity cases

Key risk factors and mitigation strategies

Property and Market Analysis:

Submarket overview with supply and demand fundamentals

Competitive set analysis with positioning matrix

Property condition assessment and capital needs

Operational improvement opportunities

Financial Analysis:

Sources and uses of funds

Pro forma income and expense projections

Cash flow waterfall and equity multiple calculations

Sensitivity tables showing downside protection

Automated investment memo creation eliminates hours spent formatting PowerPoint decks and ensures consistency across all deal presentations. The software maintains direct links from memo metrics back to underlying model assumptions, enabling real-time updates when assumptions change during committee discussions.

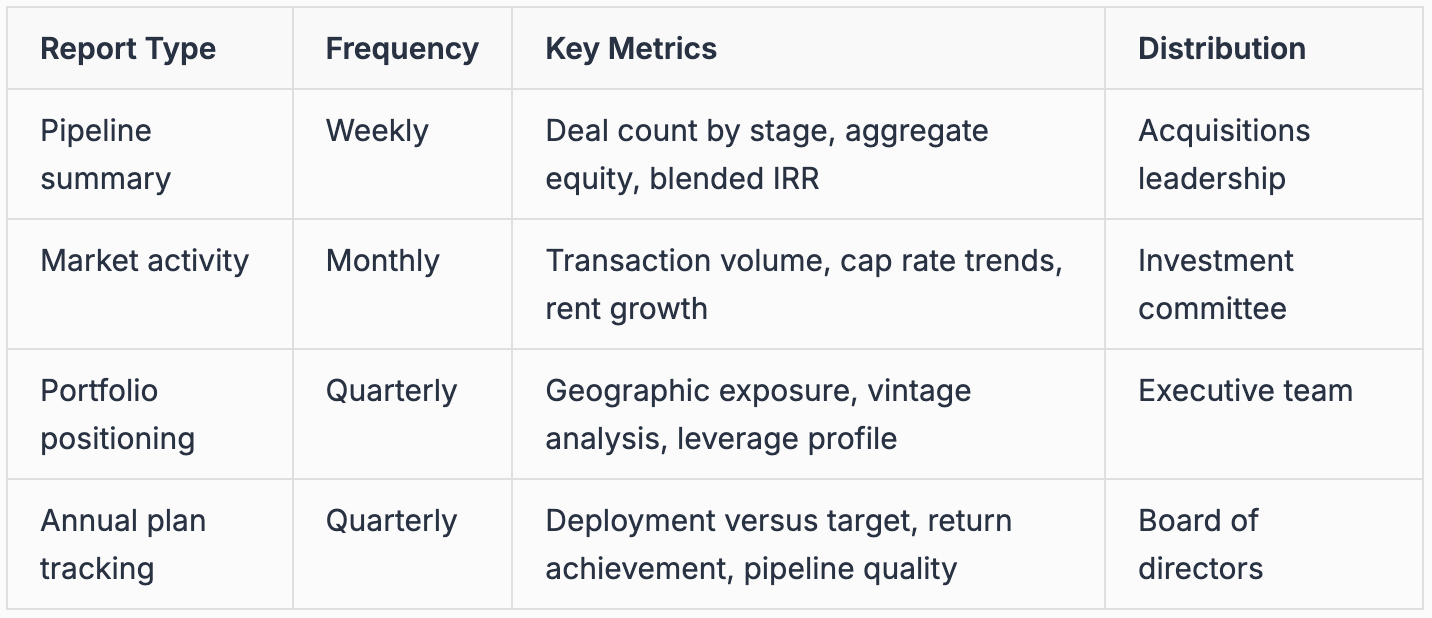

Managing Portfolio-Level Underwriting and Reporting

Acquisitions teams underwriting multiple opportunities simultaneously need portfolio visibility. Your multifamily underwriting software should aggregate deal-level metrics into portfolio dashboards showing pipeline status, projected deployment timing, and blended return profiles.

Track each opportunity's progression through underwriting stages: initial screening, full underwriting, LOI submission, due diligence, and investment committee approval. Classify deals by vintage, submarket, and investment strategy to identify portfolio concentration risks.

Portfolio Reporting Requirements

Recurring portfolio reporting demands automation. AI-powered reporting tools generate these deliverables on scheduled intervals, pulling current data from active underwriting models without manual analyst intervention.

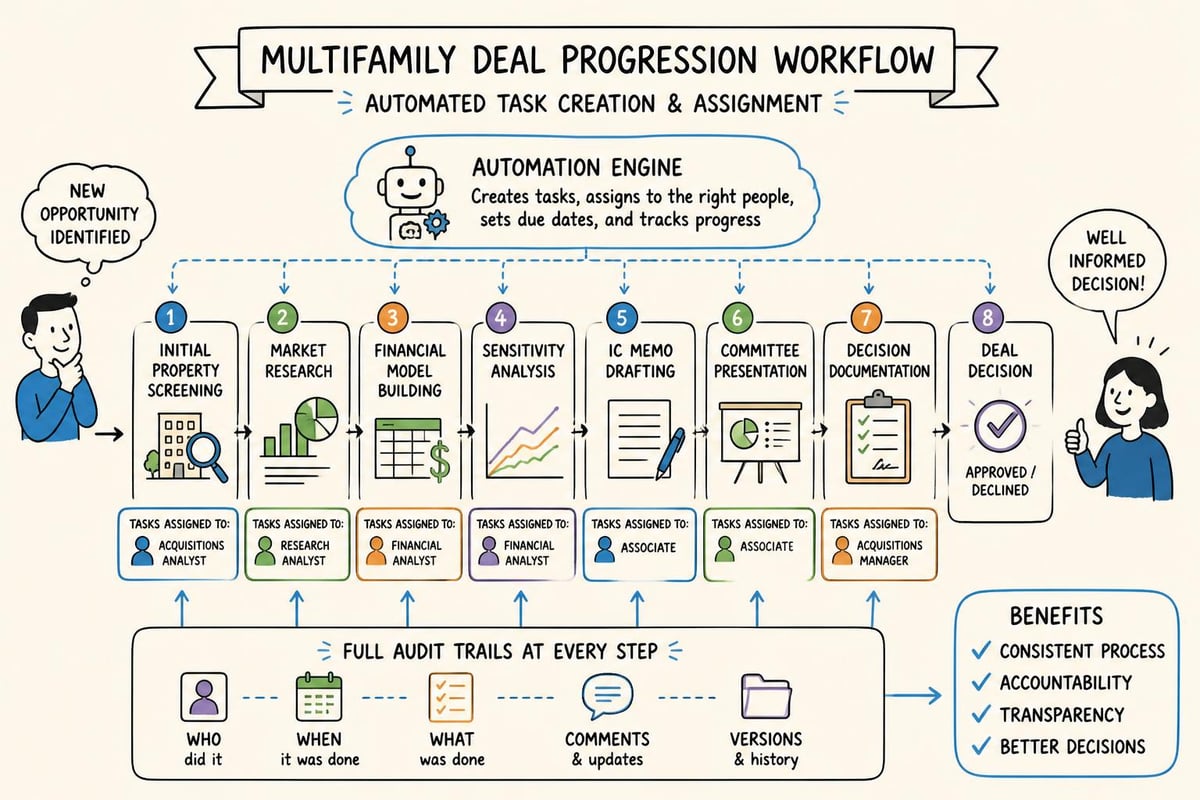

Implementing Workflow Automation and Task Management

Underwriting involves repeatable processes that benefit from standardization. Define workflow templates specifying required analyses, approval gates, and documentation standards. Your multifamily underwriting software should enforce these templates while accommodating property-specific requirements.

Automated task assignment ensures accountability. When a new deal enters the pipeline, the system creates tasks for market research, rent roll analysis, financial modeling, and memo drafting. Track completion status and flag bottlenecks delaying deal progression.

Standard Underwriting Workflow Steps

Initial Screening: Review offering memorandum, calculate back-of-envelope returns, determine pursuit decision

Detailed Market Research: Analyze submarket fundamentals, compile transaction and rental comps, assess competitive positioning

Financial Modeling: Build base case pro forma, create sensitivity matrices, calculate return metrics

Risk Assessment: Identify key risks, quantify downside scenarios, develop mitigation strategies

IC Memo Preparation: Draft investment narrative, compile supporting exhibits, prepare presentation materials

Committee Review: Present analysis, address questions, document decision and feedback

Post-Decision Actions: Execute LOI if approved, archive analysis if passed, update pipeline tracking

The platform should maintain complete audit trails showing who performed each step and when. This documentation proves essential during portfolio reviews and investor reporting cycles. Financial modeling and underwriting platforms purpose-built for real estate understand these workflow requirements rather than forcing CRE teams into generic project management tools.

Ensuring Data Security and Compliance

Multifamily underwriting involves confidential financial information, proprietary market intelligence, and non-public acquisition targets. Your software must provide enterprise-grade security controls protecting this sensitive data.

Evaluate platforms based on their security certifications. SOC 2 Type 2 compliance demonstrates the vendor maintains appropriate controls for data security, availability, and confidentiality. This certification requires independent auditor verification of security practices over an extended evaluation period.

Essential Security Features:

Role-based access controls limiting data visibility by job function

Encryption for data at rest and in transit

Multi-factor authentication for all user accounts

Comprehensive activity logging for audit purposes

Regular security penetration testing and vulnerability assessments

Data residency requirements matter for firms operating across multiple jurisdictions. Confirm whether your underwriting data resides in specific geographic regions and how the vendor handles cross-border data transfers.

Selecting the Right Platform for Your Organization

Platform selection requires evaluating both immediate needs and long-term scalability. Start by documenting your current underwriting volume, team size, and portfolio complexity. Project how these factors will evolve over your strategic planning horizon.

Evaluation Criteria Framework

Functional Requirements:

Financial modeling depth and calculation accuracy

Document extraction capabilities across file formats

Market research integration and data sources

Sensitivity analysis flexibility and automation

IC deliverable generation and customization

Portfolio aggregation and reporting functionality

Technical Requirements:

Property management system connectivity

Excel compatibility for legacy model migration

API access for custom integrations

Mobile accessibility for field use

Uptime guarantees and disaster recovery plans

Vendor Considerations:

Implementation timeline and resource requirements

Training programs and documentation quality

Customer support responsiveness and expertise

Product roadmap alignment with CRE trends

Financial stability and client retention rates

Request detailed product demonstrations using your actual deal data. Generic demos with sample properties rarely reveal platform limitations. Test edge cases like properties with complex lease structures, mixed-use components, or unusual financing arrangements.

Transitioning From Excel to Integrated Platforms

Excel remains ubiquitous in commercial real estate underwriting, but its limitations compound as portfolio complexity grows. Spreadsheets lack built-in version control, collaboration features, and audit trails. Formula errors propagate silently, and linking across multiple workbooks creates brittle dependencies.

Migration from Excel-based workflows to dedicated multifamily underwriting software requires careful planning. Begin by standardizing your existing Excel templates before attempting platform transition. Document calculation methodologies, assumption hierarchies, and output requirements.

Run parallel processes during initial implementation. Continue Excel-based underwriting while simultaneously building models in the new platform. Compare outputs to validate the software accurately replicates your calculation logic. This parallel approach builds confidence before fully committing to the new system.

Migration Best Practices:

Start with new deals rather than converting in-flight underwriting

Create a template library matching your existing Excel structure

Train power users first to develop internal expertise

Document platform-specific workflows and shortcuts

Establish data governance policies from day one

Schedule regular check-ins during the first ninety days

Modern platforms offer Excel integration rather than requiring complete abandonment of familiar tools. Generate detailed underwriting models within the platform, then export to Excel for final formatting or specialized analyses. This hybrid approach leverages each tool's strengths.

Leveraging AI for Underwriting Automation

Artificial intelligence transforms multifamily underwriting by automating repetitive analytical tasks. AI-powered real estate platforms extract data from rent rolls and operating statements, generate financial models following your firm's standards, and draft initial investment memos.

The technology excels at handling multi-step workflows that traditionally consume hours of analyst time. Point the AI at a confidential information memorandum, and it extracts property details, builds a base case pro forma, researches comparable transactions, and assembles a preliminary investment memo. Analysts review and refine these outputs rather than creating them from scratch.

Real estate-native AI reasoning differs fundamentally from general-purpose language models. Purpose-built platforms understand T12 reconciliation logic, recognize when rent rolls contain unusual terms requiring adjustment, and apply appropriate underwriting conventions for multifamily versus other asset classes.

AI-Driven Underwriting Capabilities

Document Intelligence:

Extract unit mix and rental data from non-standard rent roll formats

Identify key terms and assumptions from offering memorandums

Parse historical financials across different accounting presentations

Flag inconsistencies between seller-provided documents

Financial Analysis:

Generate complete underwriting models from extracted data

Calculate returns under multiple debt structure scenarios

Produce sensitivity tables testing key assumption ranges

Identify value-add opportunities through NOI optimization

Research Integration:

Compile market comps from transaction databases

Analyze demographic and employment trends in property submarket

Track comparable property performance and rental surveys

Link model assumptions to supporting research sources

Deliverable Creation:

Draft investment committee memos following firm templates

Generate executive summaries highlighting key decision factors

Create presentation decks with supporting charts and tables

Maintain source links from outputs back to underlying data

Automated lease data processing demonstrates AI's potential in multifamily contexts. Rather than manually entering hundreds of lease records, the platform reads lease agreements, extracts critical dates and economics, and populates rent roll databases automatically.

Connecting Underwriting to Asset Management

Underwriting assumptions become asset management targets post-acquisition. Effective multifamily underwriting software bridges the acquisition-to-operations handoff by preserving deal models as performance benchmarks. Track actual results against underwriting projections to refine future deal assumptions.

Integration with property management systems enables seamless transition from underwriting to asset management. The same platform handling pre-acquisition analysis should ingest actual operating data, compare performance to pro forma projections, and highlight variances requiring attention.

Build feedback loops improving underwriting accuracy over time. When actual renovation costs exceed budgets or lease-up timelines extend beyond projections, document these variances and adjust future deal assumptions. Organizations that systematically learn from past performance develop significant competitive advantages in deal evaluation.

Post-Acquisition Analysis Components:

Variance reporting comparing actuals to underwriting assumptions

Updated return projections incorporating current performance

Business plan tracking for capital improvements and operational initiatives

Refinancing analysis testing optimal timing and structure

Disposition modeling evaluating hold-versus-sell decisions

Portfolio analytics platforms connect underwriting precision to operational execution, creating continuous improvement cycles that enhance both acquisition discipline and asset management performance.

Successful multifamily underwriting requires sophisticated software that automates data extraction, standardizes financial modeling, integrates market research, and generates investment committee deliverables while maintaining complete audit trails. Organizations evaluating platforms must prioritize real estate-native functionality over generic financial tools. Leni serves as an AI analyst platform purpose-built for these exact workflows, handling financial modeling, document extraction, IC memo creation, and portfolio reporting through autonomous, long-running tasks that connect directly to property management systems and deliver verifiable outputs with source links. Teams seeking to eliminate manual underwriting bottlenecks while improving analytical accuracy should explore how purpose-built platforms transform their deal evaluation processes.

Johanna Gruber

Johanna has spent the last 8 years helping marketing teams connect with audiences through content. Specializing in B2B SaaS and real estate.

Curious About AI?

Join the largest AI community for real estate online. Get bite-sized, real-world use case videos, plus practical tips and proven strategies from top industry experts on adopting AI effectively.

MEET LENI

AI SuperAgent Purpose Built for Investors and Operators.

Experience how professionals and teams in your domain are getting the edge using AI.